If you own a U.S. single-member LLC as a non-resident, the 5472 filing is not optional

Non-residents who form a U.S. single-member LLC that is treated as a disregarded entity have an annual IRS filing requirement that most sellers do not know about until it is too late.

The penalty for missing it starts at $25,000 per form, per year. There is no maximum. And the IRS does not care that nobody told you.

What the filing requirement is

When a non-resident owns a U.S. single-member LLC that is a disregarded entity, and there are reportable transactions between the LLC and its foreign owner, the LLC must file Form 5472 attached to a pro forma Form 1120 with the IRS every year.

This is an information return, not a tax return. It reports the transactions between related parties. The IRS uses it to verify that money moving between your U.S. entity and your foreign company or personal accounts is properly documented and priced.

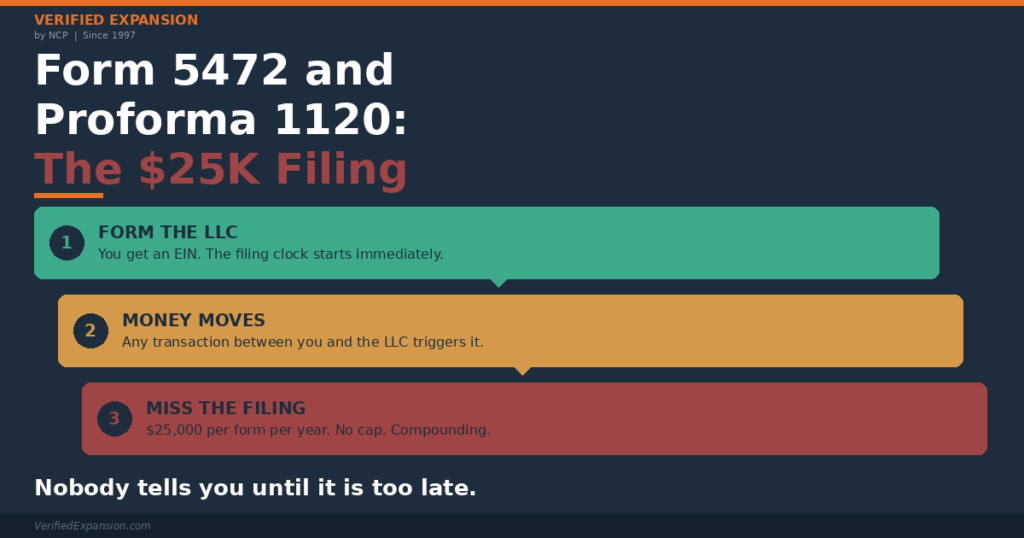

The filing is triggered the year after you form the LLC and obtain an EIN. If you formed a U.S. LLC and have been operating it without filing, the clock has been running.

Why does this catch sellers off guard

Most formation companies do not mention it. Most YouTube guides skip it entirely. The marketplace that required you to form the LLC does not remind you.

You form the LLC. You get the EIN. You start selling. Nobody tells you about the annual filing until a CPA asks for it or the IRS sends a notice.

By then, you may owe $25,000 or more in penalties for each year you missed, and you need a tax professional to file late returns and request penalty abatement.

What triggers the filing

Any reportable transaction between the U.S. LLC and its foreign owner or any foreign related party triggers the requirement. This includes capital contributions, loans, payments for services, distributions, and management fees.

If money moved between you and your U.S. LLC in any direction, the filing is almost certainly required.

The form must be consistent with your LLC’s classification, the way your EIN application was completed, and the nature of your actual transactions. When these tell different stories, the problems multiply.

The penalty is severe and compounded

The IRS imposes a $25,000 penalty for each Form 5472 filed late. If the IRS sends a notice and you still do not file within 90 days, an additional $25,000 penalty accrues for each month of continued failure.

There is no cap. Sellers who miss two or three years can face penalties of $50,000 to $75,000 or more before they even realize the requirement exists.

Penalty abatement is possible in some cases, but it requires proper filing, a reasonable-cause argument, and professional representation. It is not guaranteed.

This is not a DIY fix

The 5472 and proforma 1120 must be prepared by someone who understands how your LLC was formed, how the EIN was obtained, what transactions occurred, and how to make the filing consistent with the rest of your tax posture.

Filing it incorrectly can create new problems. The numbers must reconcile with your entity classification, your intercompany transactions, and any other returns you file.

CEO Blueprint: get the filing right

The CEO Blueprint identifies every filing obligation tied to your U.S. entity before anything is submitted.

Two calls with Scott Letourneau, MSCTA®. A written plan up to 10 pages delivered in 3 business days. Specialist matching to the right CPA who handles foreign-owned disregarded entity filings.

If you have already missed filings, Scott will map the cleanup path, including a penalty abatement strategy.

This post is educational information, not legal or tax advice. Consult a licensed CPA, tax attorney, or enrolled agent for guidance specific to your situation.