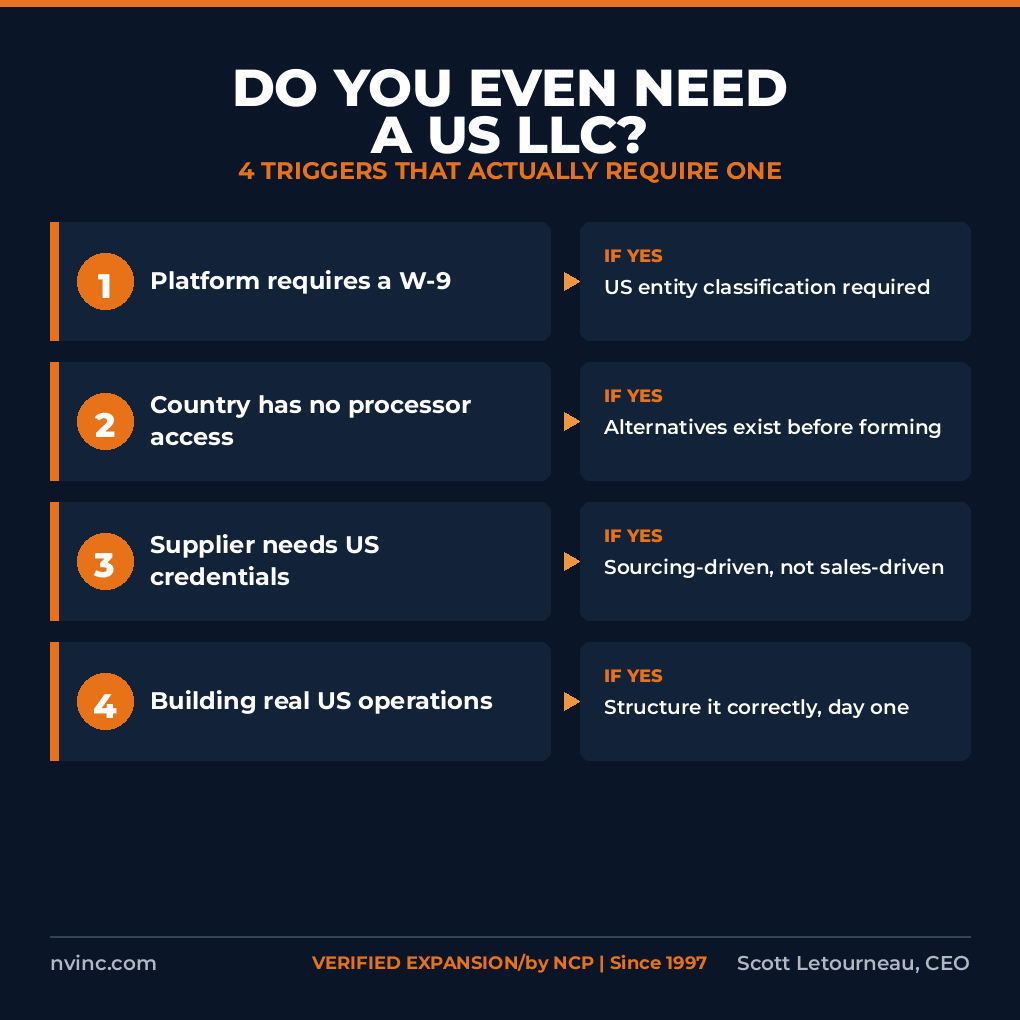

Do Non-Residents Even Need a US LLC to Sell in the U.S.?

If you’re running a seven-figure foreign-owned brand, you already know you don’t form a US LLC just to sell into the US marketplace, one of the largest in the world. The real question is which of a small number of specific triggers actually changes that. If you’re selling through a channel that requires a W-9, […]

Why Most U.S. TikTok Shop Accounts Fail Before They Ever Make a Sale

TikTok Shop approval is not a single hurdle, it is five separate checkpoints. In this guide we break down every stage where U.S. and non-resident sellers lose their accounts, from PBR KYC to bank and product risk review, and show you the structure and documentation you need in place to survive each one.

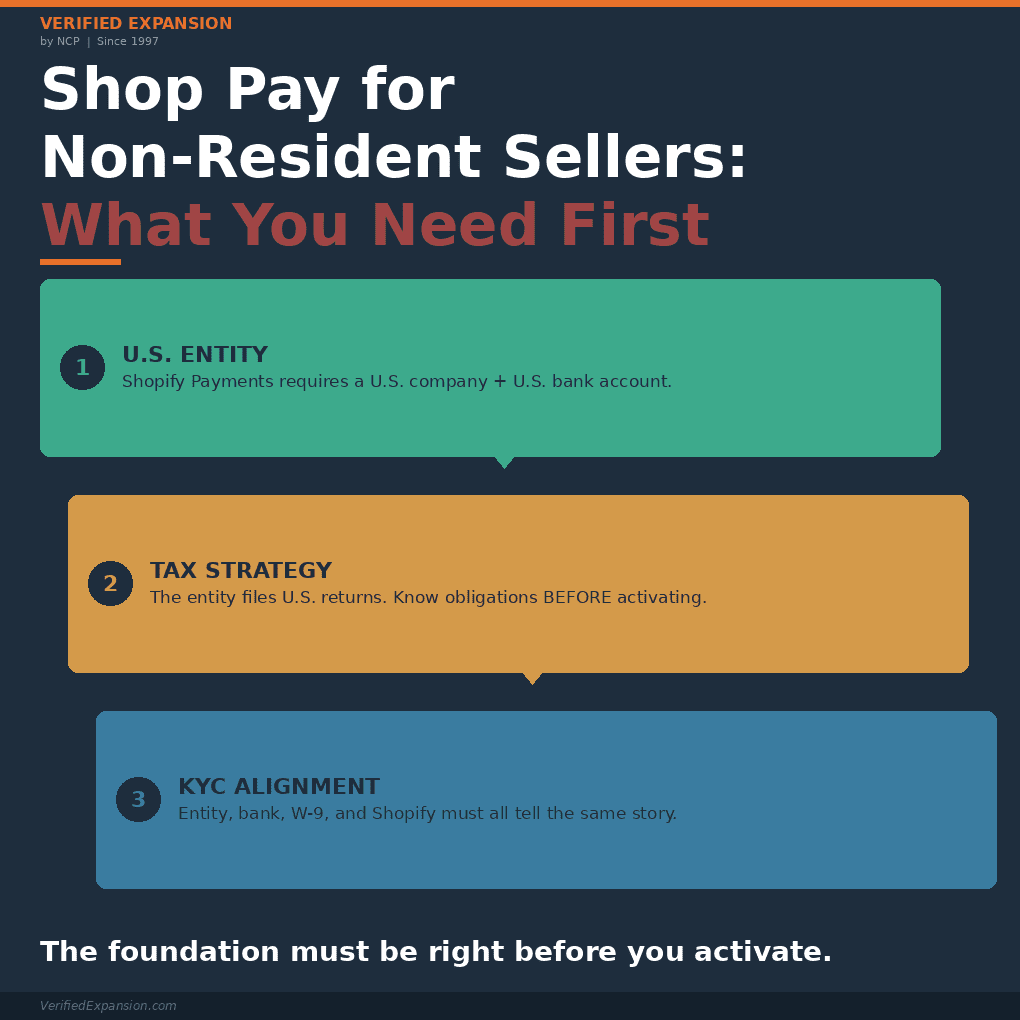

Shop Pay Secrets: The Ultimate Payment Strategy for Non-U.S. Sellers

Shop Pay is Shopify’s highest-converting checkout. Non-residents cannot access it without a U.S. entity. Shop Pay stores customer payment and shipping information for one-click purchases. It significantly increases mobile conversions and builds repeat-buyer loyalty. But Shop Pay requires Shopify Payments. And Shopify Payments requires a U.S. entity with a U.S. bank account. For non-resident sellers, […]

Shopify Payments US Is Rejecting Non-Resident Sellers (2026)

The Two Things That Stop the Old Shopify Payments Playbook If you last researched Shopify Payments US in 2024 or 2025, most of what you learned is now wrong or dangerous. Two shifts changed the game: Shopify’s operational presence enforcement got sharper. The old “form a Wyoming LLC, get an EIN, use a virtual address” […]

TikTok Shops Account Setup Changed: Why Legitimate Sellers Are Failing

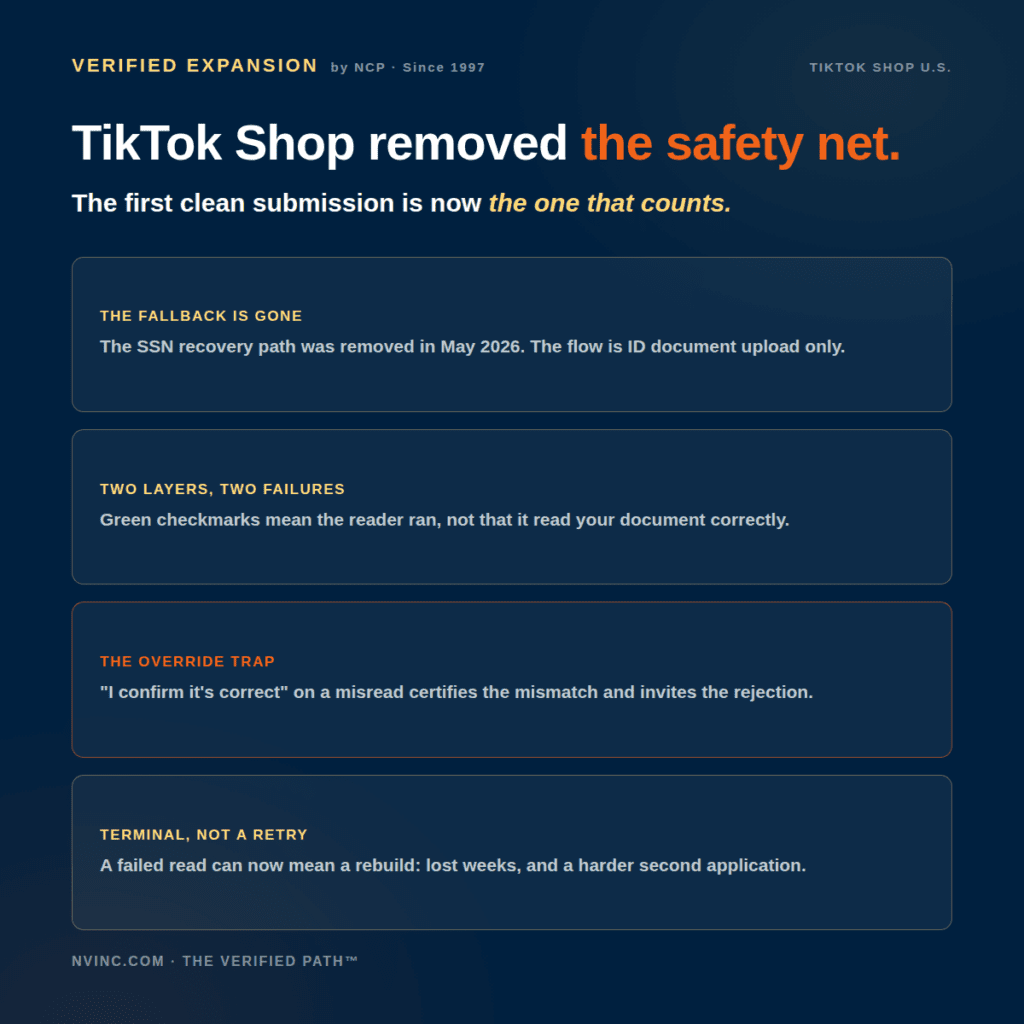

Your passport is real. Your entity’s IRS records are correct. Your documents are clean. You still got rejected on your TikTok Shop account setup. Updated July 2026. This post reflects the change to TikTok Shop’s verification flow in early-to-mid May, the two-layer reader-and-risk system that drives the failures, and TikTok’s official capture-quality instruction. If that […]

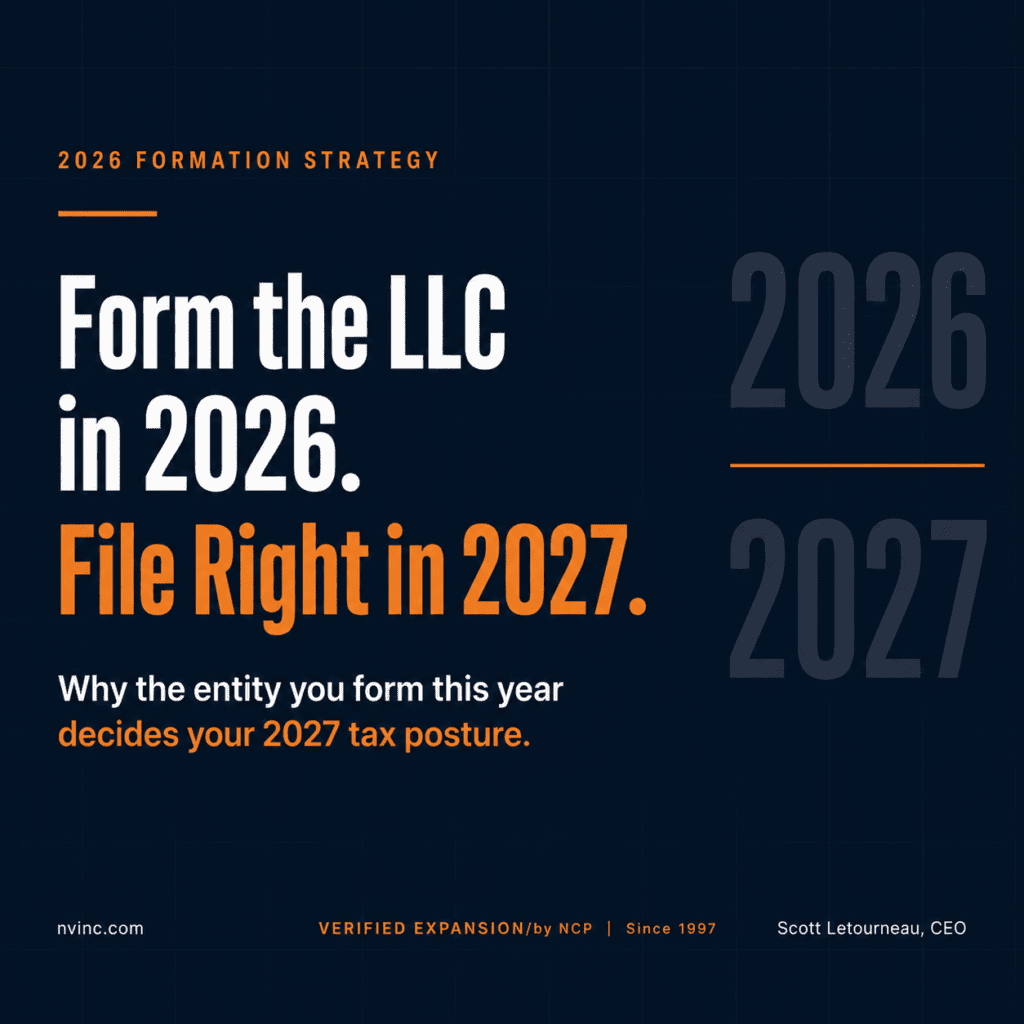

Why Forming Your LLC Now (in 2026) is the Best Move for a Powerful Start in 2027

If you’re unsure when to form your LLC, I’m here to tell you: form it now. As a certified tax advisor, I’ve seen countless entrepreneurs make the mistake of waiting until January. The logic seems sound: new year, new business, right? But here’s the problem: that approach could cost you in tax savings, compliance complications, […]

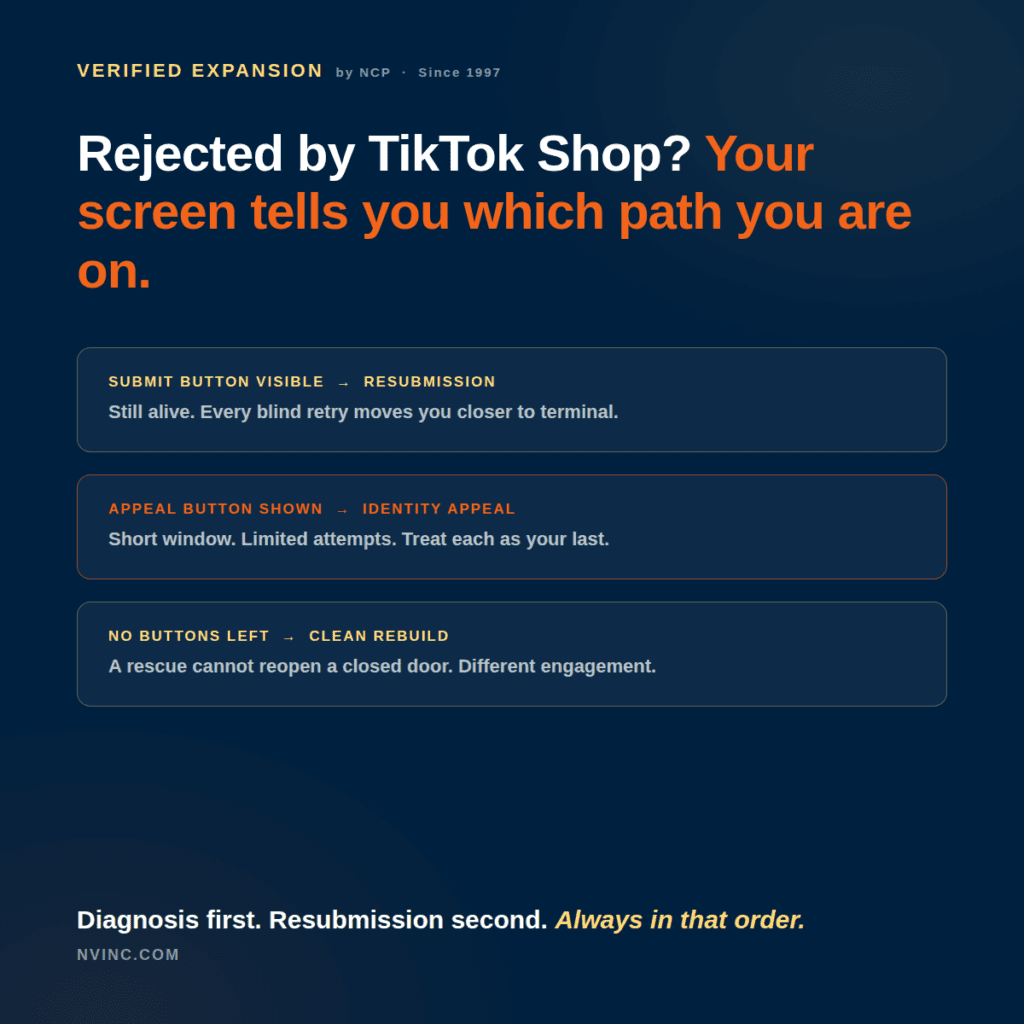

TikTok Shop Application Rejected? What to Do Before You Resubmit

You just got rejected from TikTok Shop. You are staring at a screen that gives you almost no information about why. Your product is ready. Your inventory is waiting. Your competitors are already selling. And the clock on your launch window is running. Updated July 2026. This post reflects TikTok’s current onboarding verification process, the […]

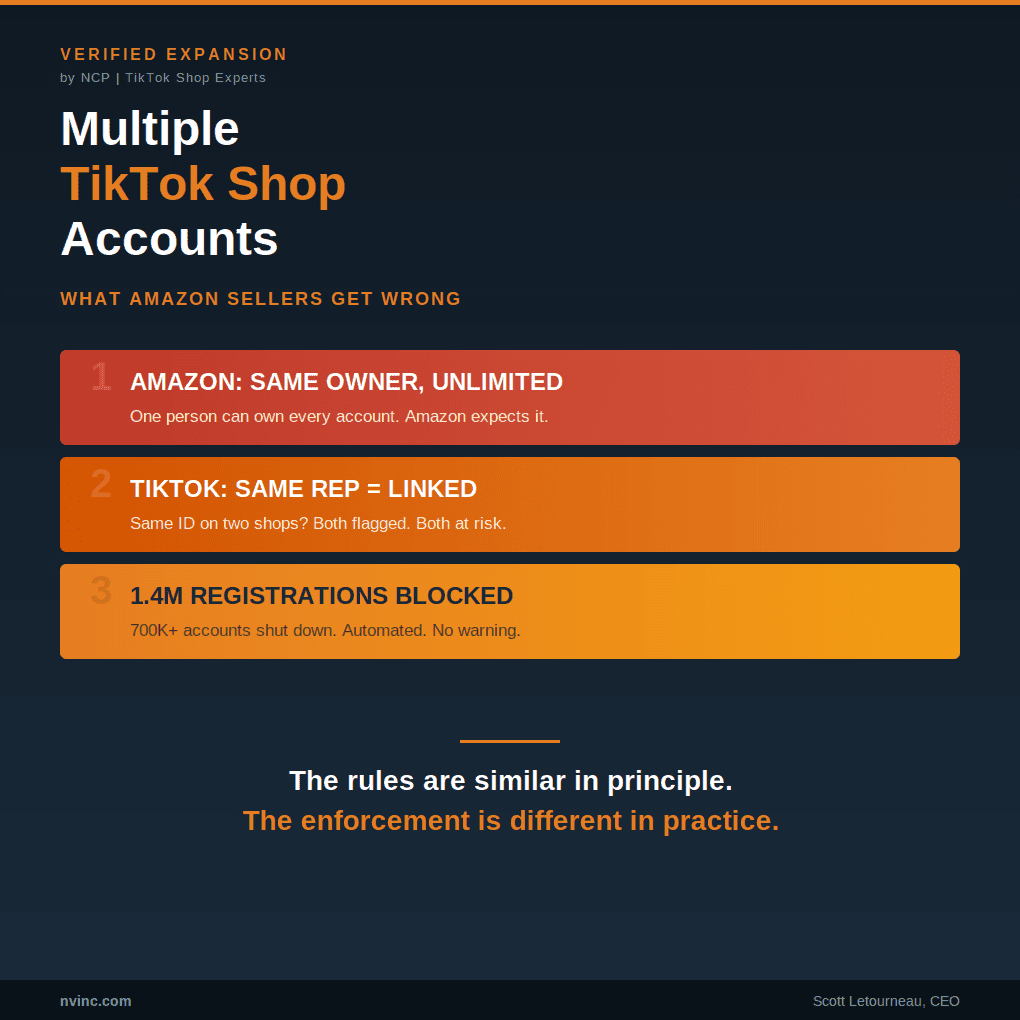

Multiple TikTok Shop Accounts: What TikTok Allows, What Gets You Banned

TikTok blocked 1.4 million seller registrations in a single six-month period. Over 700,000 active seller accounts were shut down for fraudulent activity in that same window. The detection is automated; it runs continuously and does not send a warning first. Updated April 2026. This post reflects TikTok’s current Seller Enforcement Policy, connected account detection practices, […]

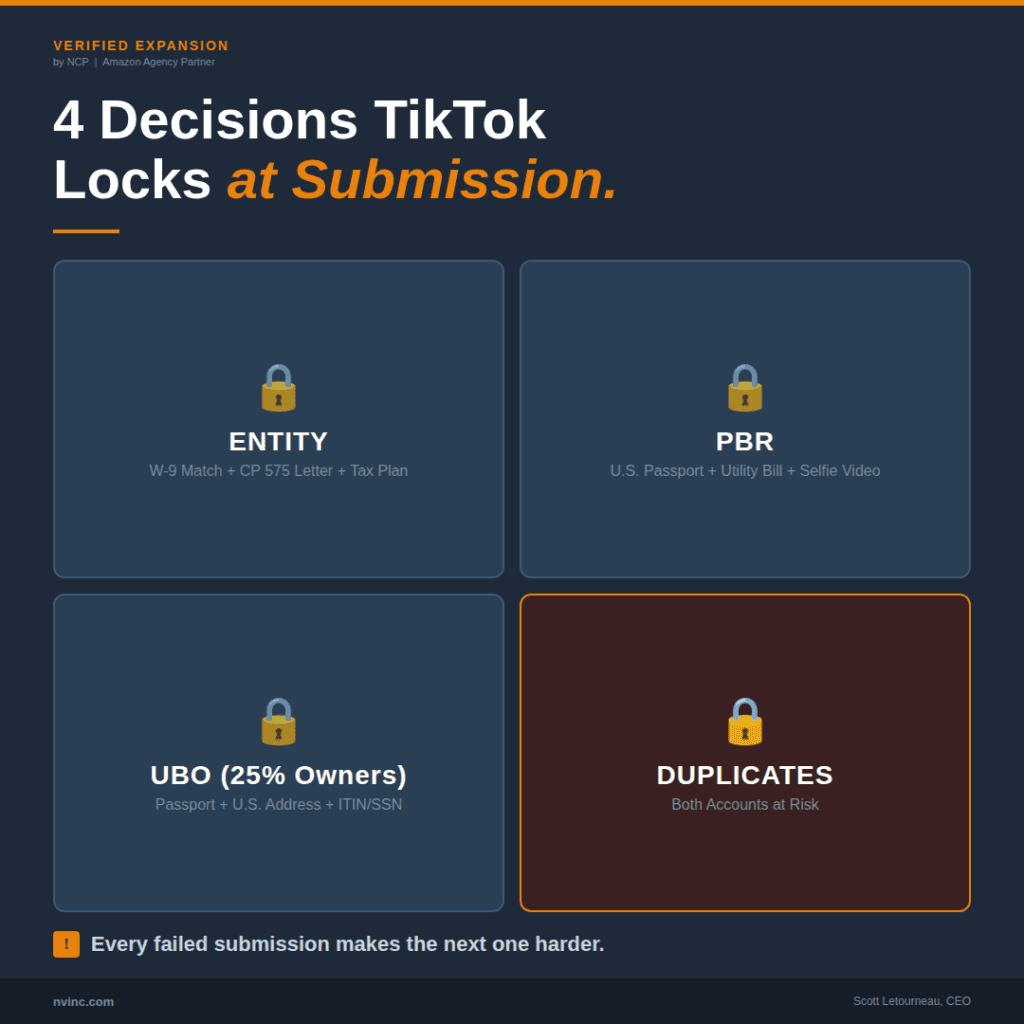

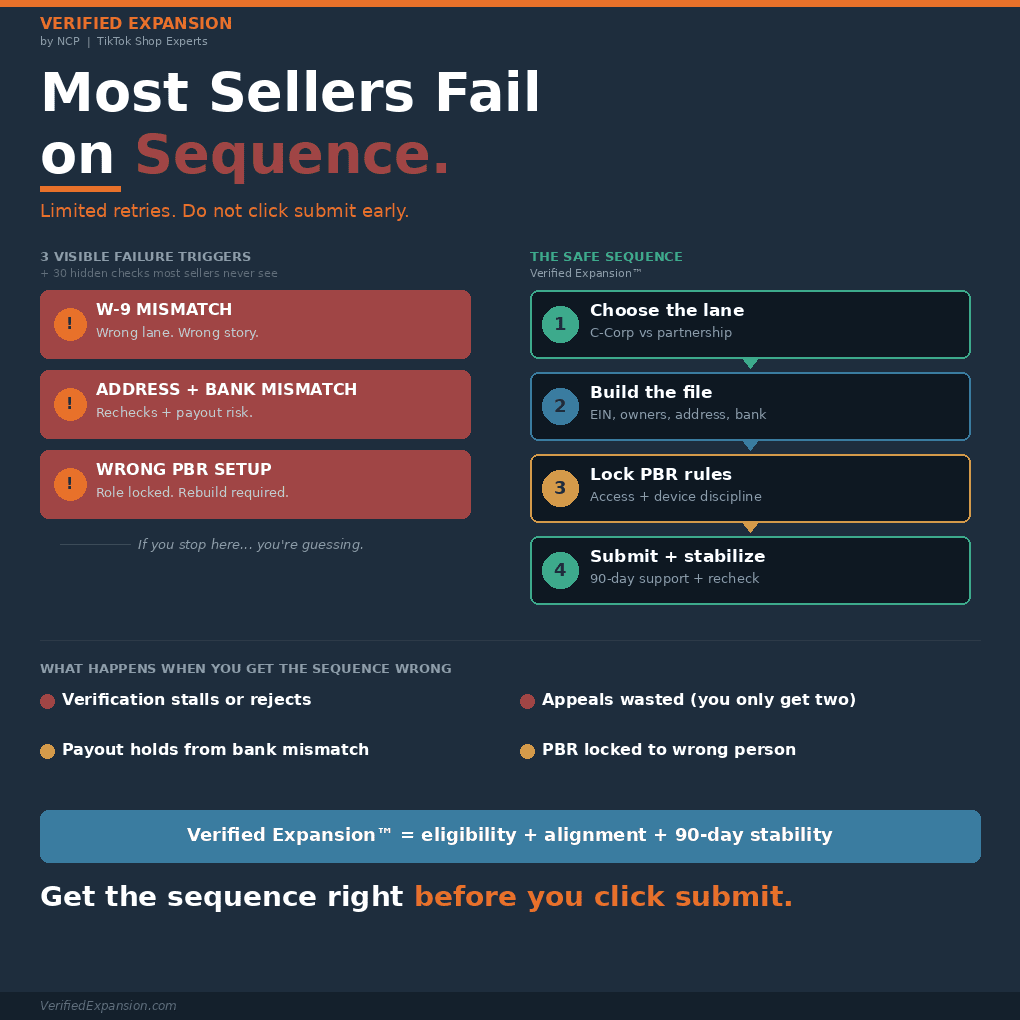

TikTok Shop Verification: The 4 Irreversible Decisions That Lock the Moment You Click Submit

Learn the compliance essentials non-U.S. residents need to know before launching on TikTok Shop, from U.S. entity structure to beneficial ownership.

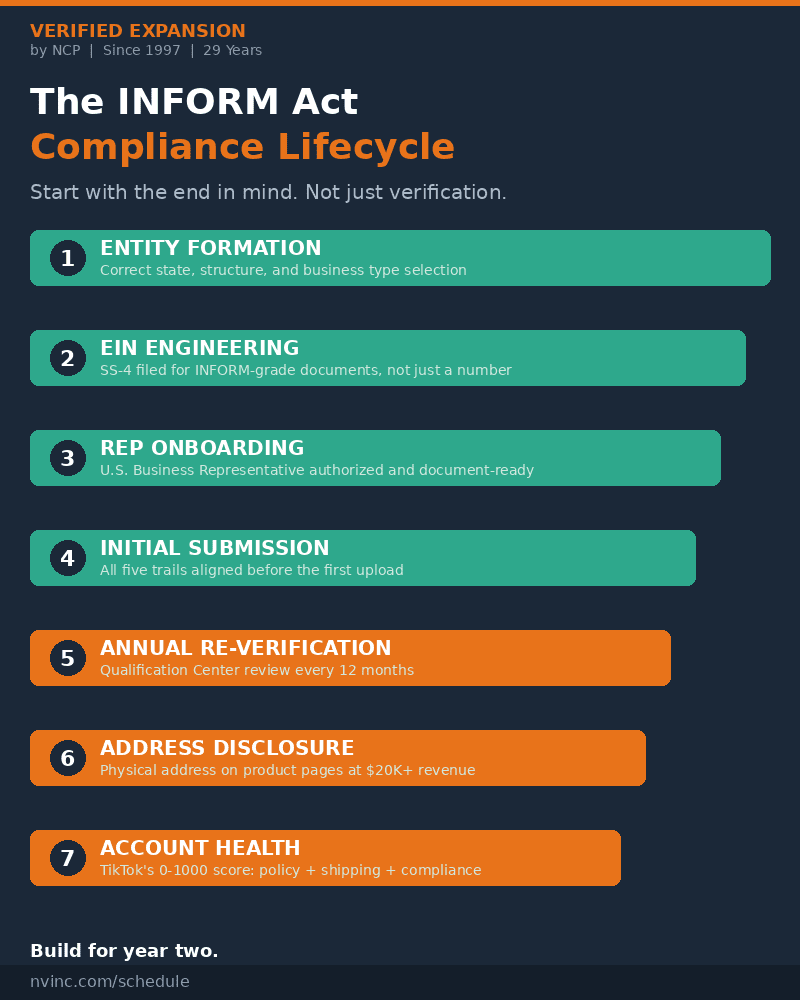

TikTok Shop INFORM Act: Why Your Shop Fails Verification

Most sellers think TikTok Shop verification fails because they uploaded the wrong file. That is not the real problem. The real problem is that TikTok no longer reviews your shop as a simple application. It is reviewing it like a compliance file. And once the INFORM Consumers Act comes into effect, the platform is under […]

Why Most TikTok Shop Brands Are Insured and Unprotected at the Same Time

You bought the TikTok Shop liability insurance policy. You filed the LLC. You launched your creator program. You are still exposed. Having a Policy Is Not the Same as Being Protected. A foreign brand forms a U.S. LLC and files it online. Applies to TikTok Shop. Activates thirty creators. Buys a product liability policy. They […]

Why TikTok Shop Verification Is Nothing Like Amazon Seller Verification

Updated March 2026: This post has been rebuilt to focus specifically on new account onboarding verification on both platforms. Content about existing-account suspensions, TOS violations, and post-verification enforcement has been removed to avoid mixing two different processes. All platform claims are grounded in Amazon’s published Seller Registration Guide and TikTok Shop’s Seller Center documentation. It […]

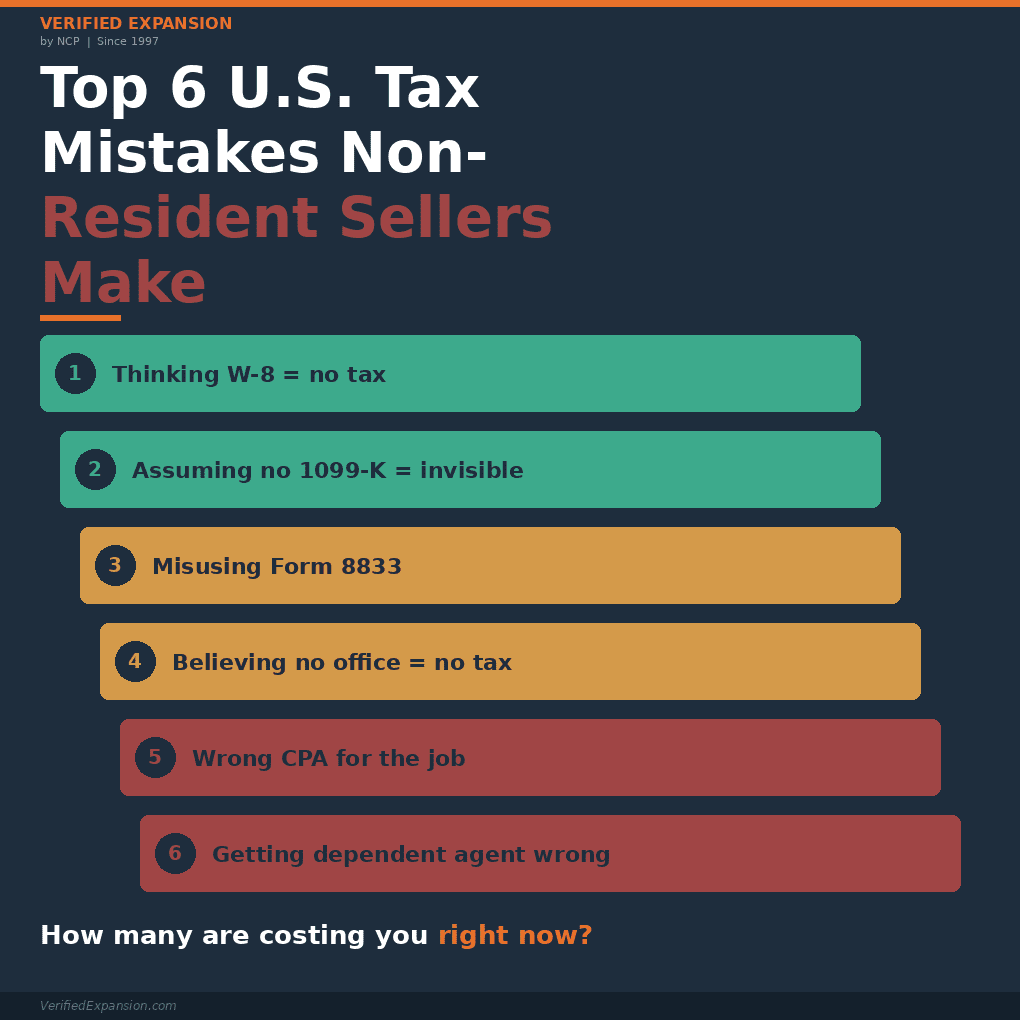

Top 6 U.S. Tax Mistakes Non-Resident Amazon Sellers Make

Six areas where non-resident sellers get U.S. tax wrong U.S. tax compliance for non-resident Amazon and TikTok Shop sellers is complex. Two sellers can run the same model and reach different outcomes. The difference comes down to U.S. activity, entity structure, and filing posture. Here are the six areas where confusion leads to penalties, overpayment, […]

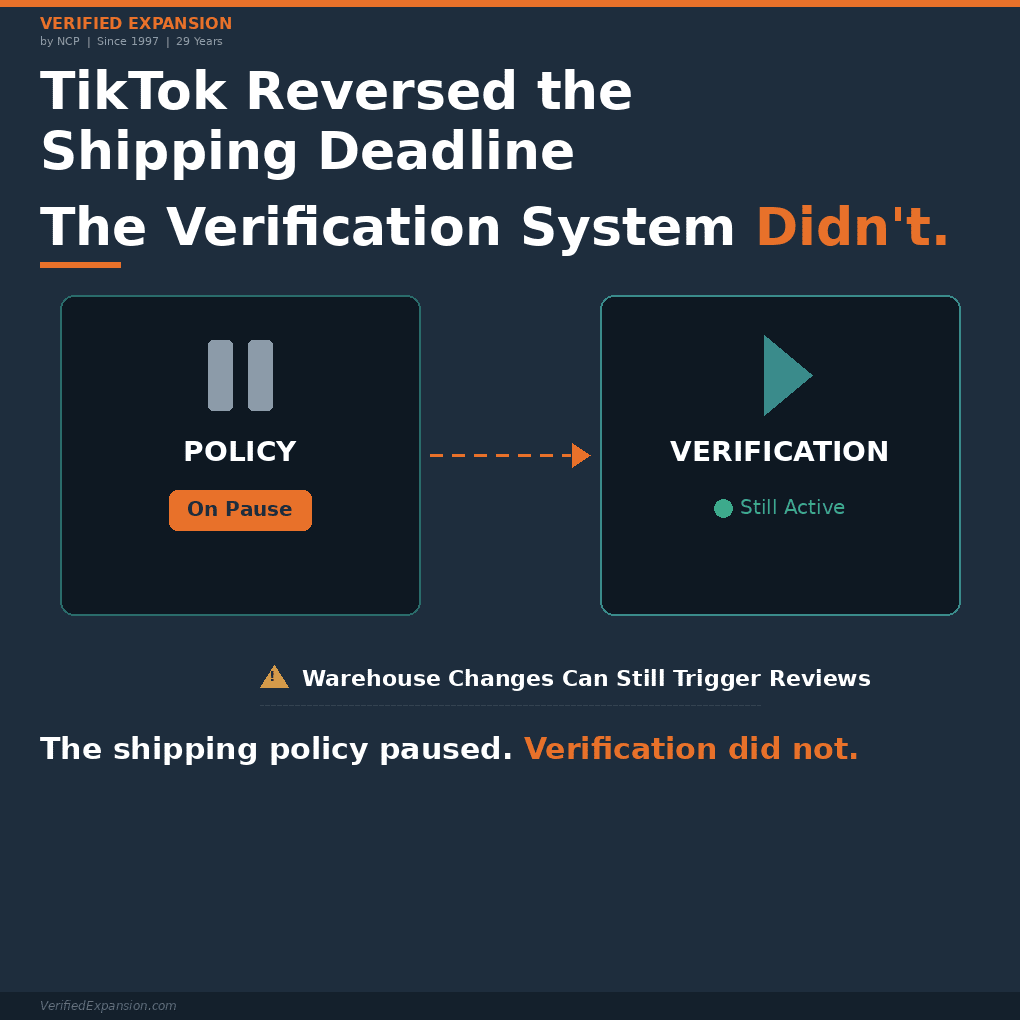

TikTok Shop Warehouse Verification: Why Shipping Changes Trigger Verification Holds

Update (February 18, 2026): TikTok Shop has reversed its Seller Shipping policy change. Previously shared deadlines are not going into effect. Sellers can continue operating as usual. But the verification system didn’t pause with it. This post explains why a simple settings change can still trigger verification requests you cannot satisfy, and how to avoid […]

TikTok Shop Verification and Joint Venture Updates for 2026

If you are building on TikTok Shop U.S., you already know the truth. Growth is real. Verification is the gate.For many founders, especially with foreign ownership, the hesitation is not about paperwork. It is about trust.Who holds my business and identity data, and what happens if the platform becomes politically unstable?This week, TikTok publicly announced […]

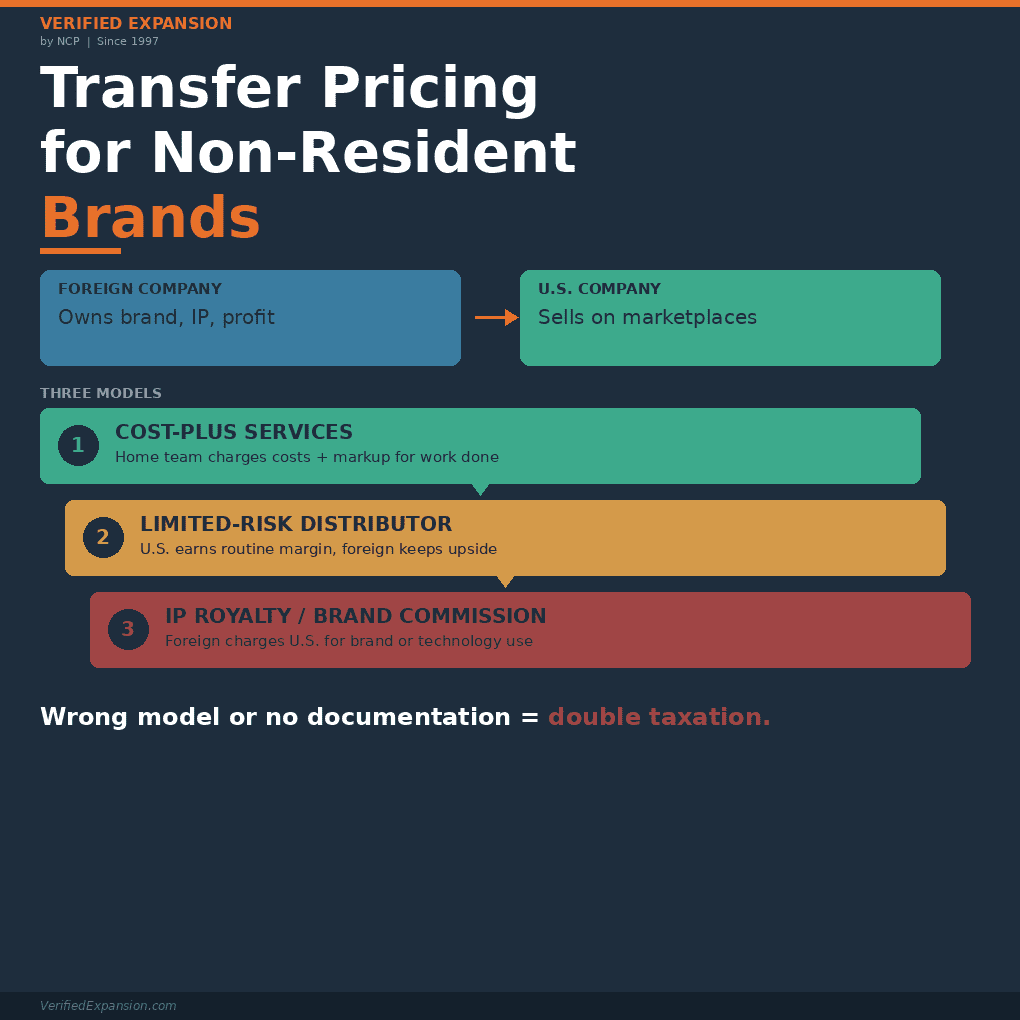

Transfer Pricing For Non-Resident Brands

For non-resident brands selling through a U.S. entity, transfer pricing is not theory, it is the engine of your tax and customs outcome. In this article we walk through a practical limited-risk distributor model, target margin ranges, and the documentation you need so your structure stands up to both IRS and CBP scrutiny.

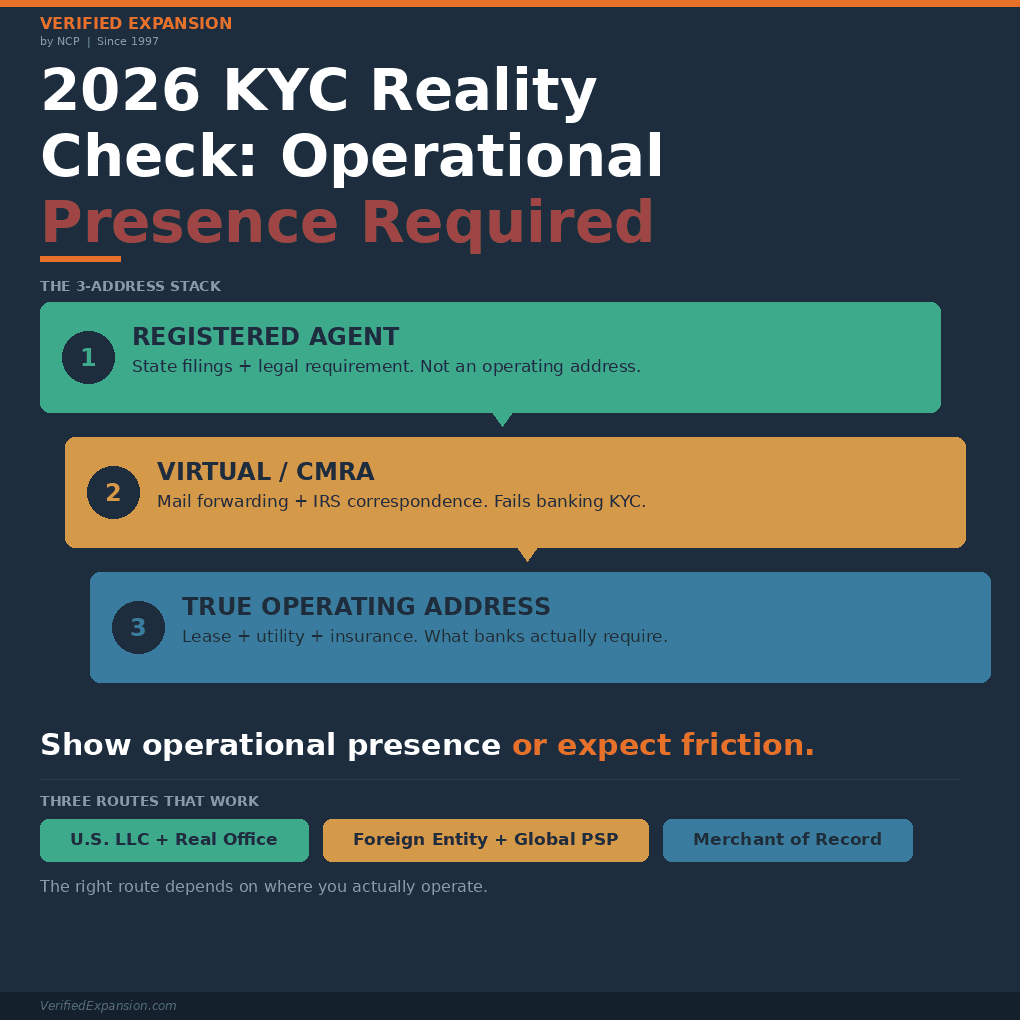

2026 KYC Reality Check: Why Non-Resident Sellers Need a U.S. Operational Presence

This diagnostic maps your best U.S. setup, outlines the exact documents banks and processors expect, and syncs your KYC, tax, and transfer pricing so nothing breaks at scale.

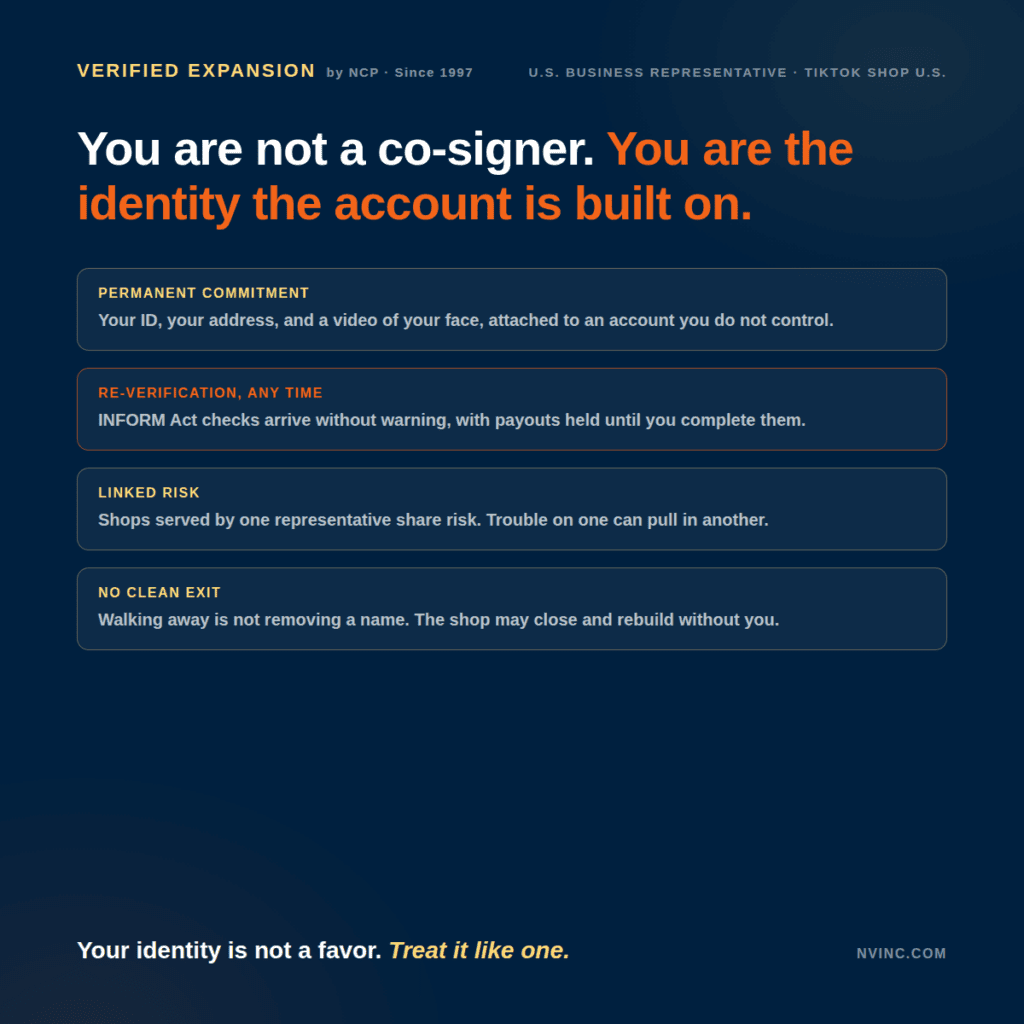

Should You Be the U.S. Business Representative for Someone’s TikTok Shop?

Someone asked you to be their U.S. Business Representative on TikTok Shop. Think carefully before you say yes. It sounds simple. Help a friend, a client, or a business partner get verified on TikTok Shop by serving as their U.S. Business Representative. You enter your information, they get approved, and everyone moves on. That is […]

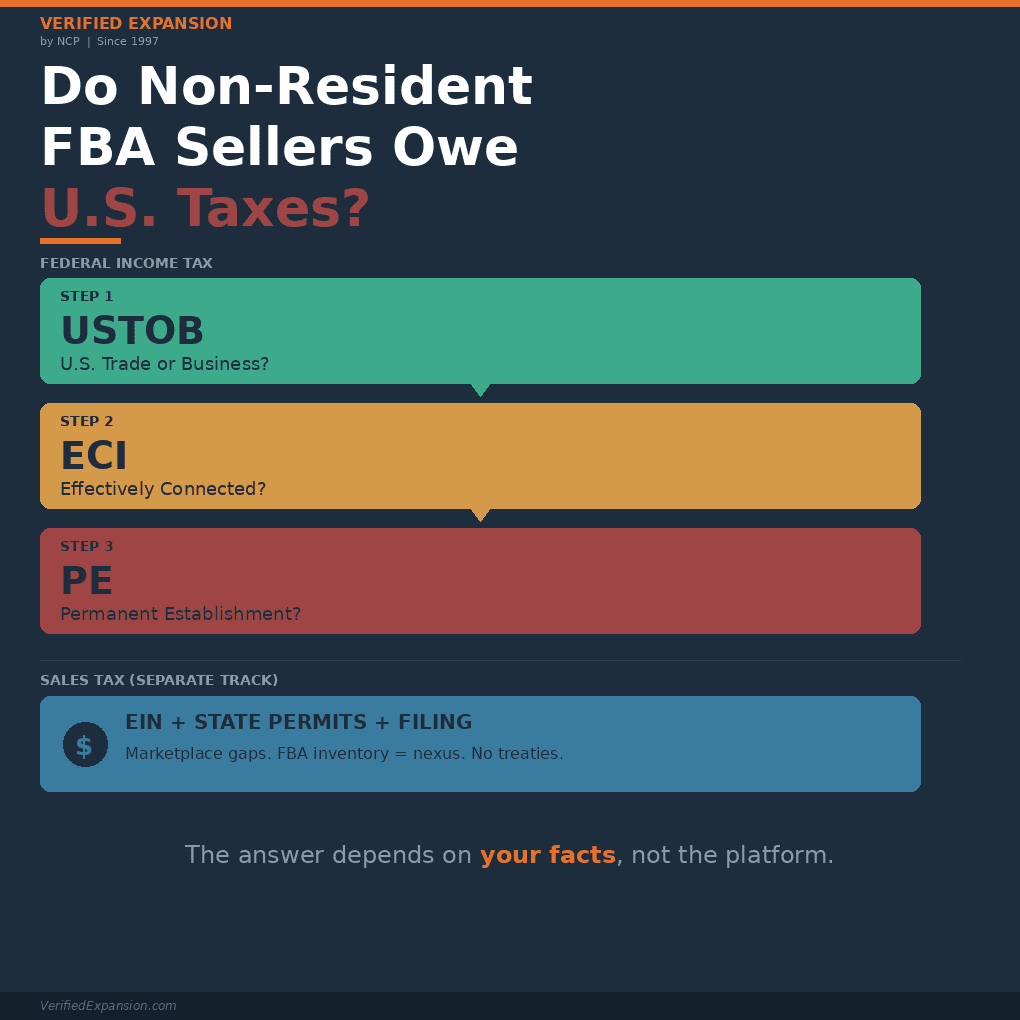

Do Non-U.S. Amazon FBA Sellers Owe U.S. Taxes?

The short answer: it depends on your U.S. activity, not the platform There is no blanket yes or no. Two sellers can run the same FBA model and reach different tax outcomes. The difference comes down to three things: how much U.S. activity you actually have, what entity structure you chose, and whether you filed […]

U.S. Taxation for Non-Resident Amazon Sellers: Why Opinions Differ

Navigating U.S. tax for non-resident Amazon sellers Navigating U.S. tax as a non-resident Amazon seller turns on two domestic tests first, then a treaty filter. The correct order is simple. Decide whether you are engaged in a U.S. trade or business (USTOB). If yes, decide whether your profit is effectively connected income (ECI). Only then […]

U.S. Business Tax Returns and Due Dates

What This Post Will Cost You If You Ignore It A foreign-owned single-member LLC that misses one Form 5472 filing owes the IRS $25,000. Automatically. No warning. No grace period. A partnership with foreign partners that fails to file on time? $255 per partner, per month, for up to 12 months. That adds up fast. […]

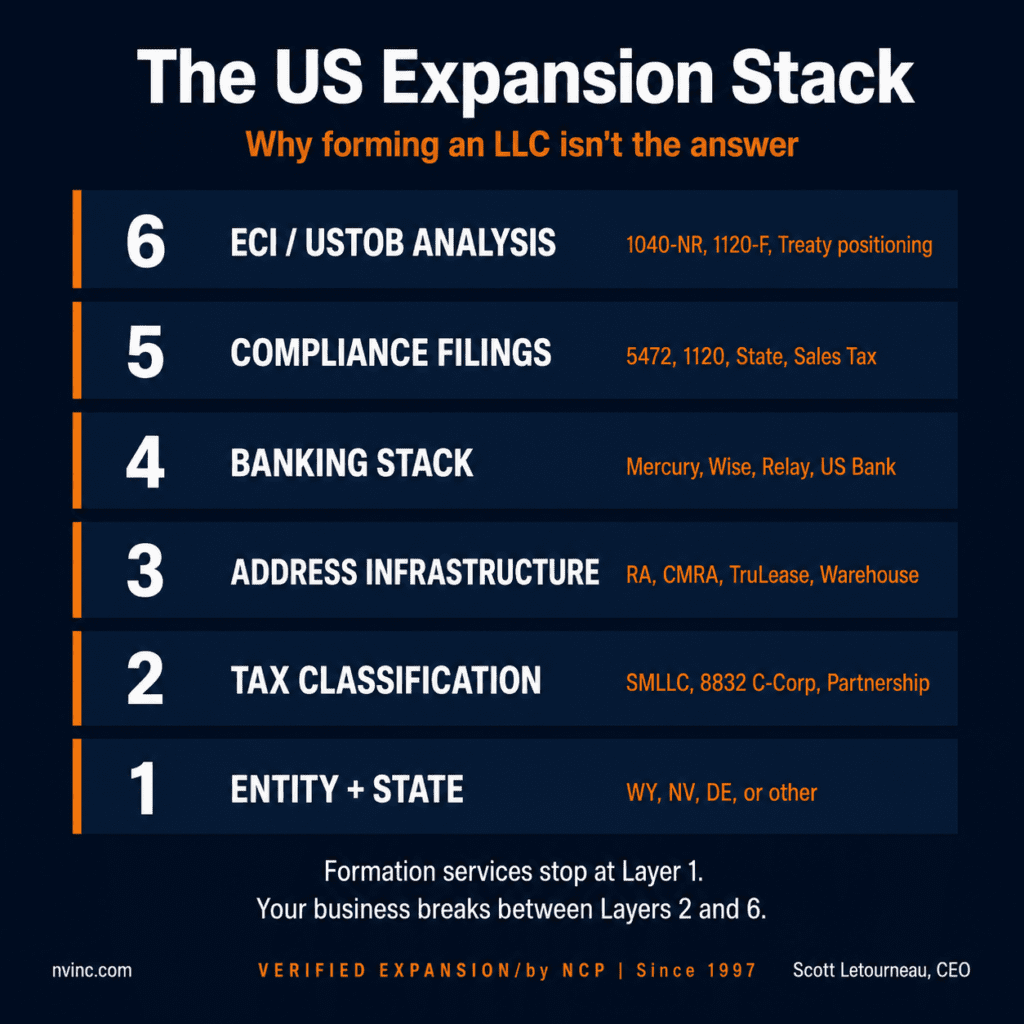

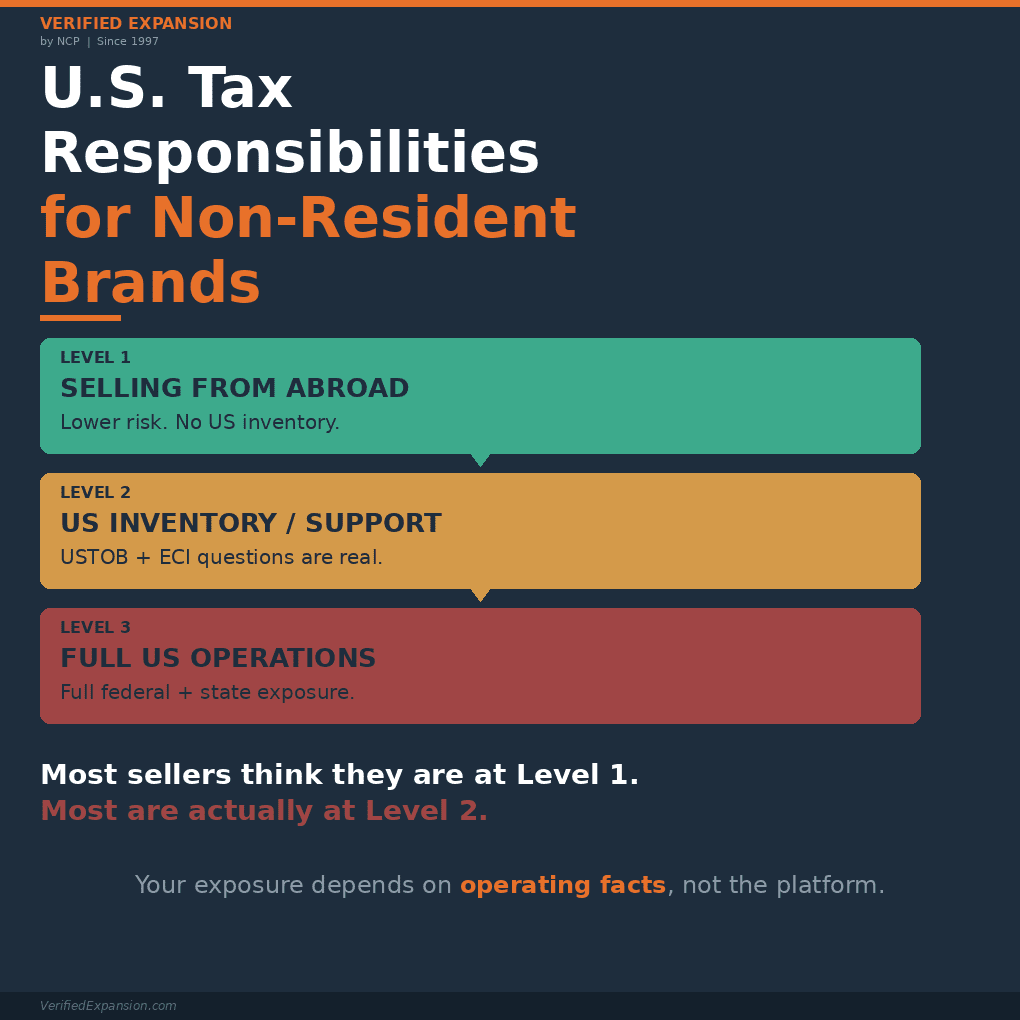

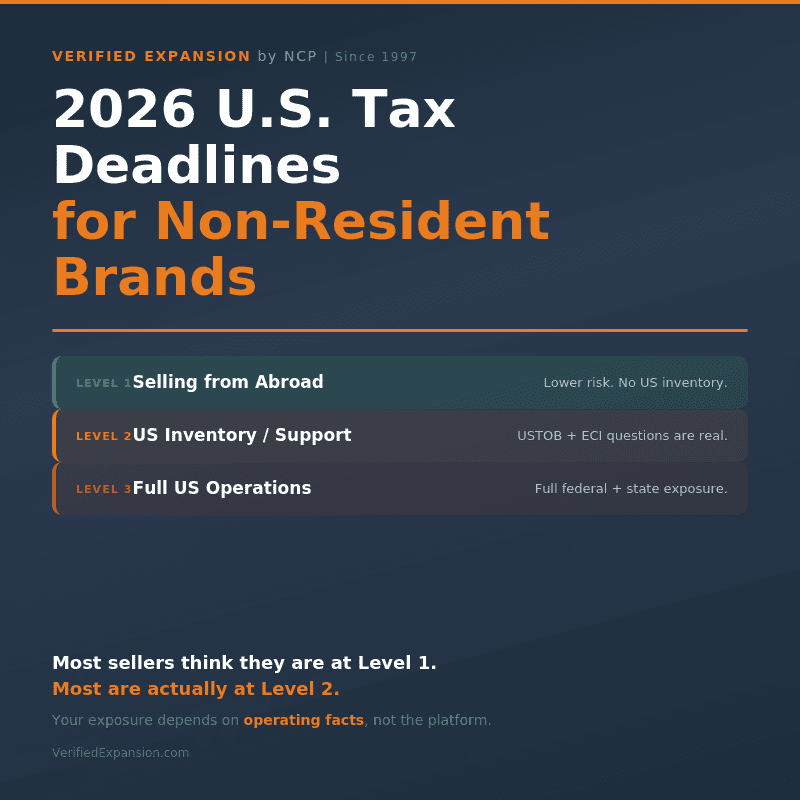

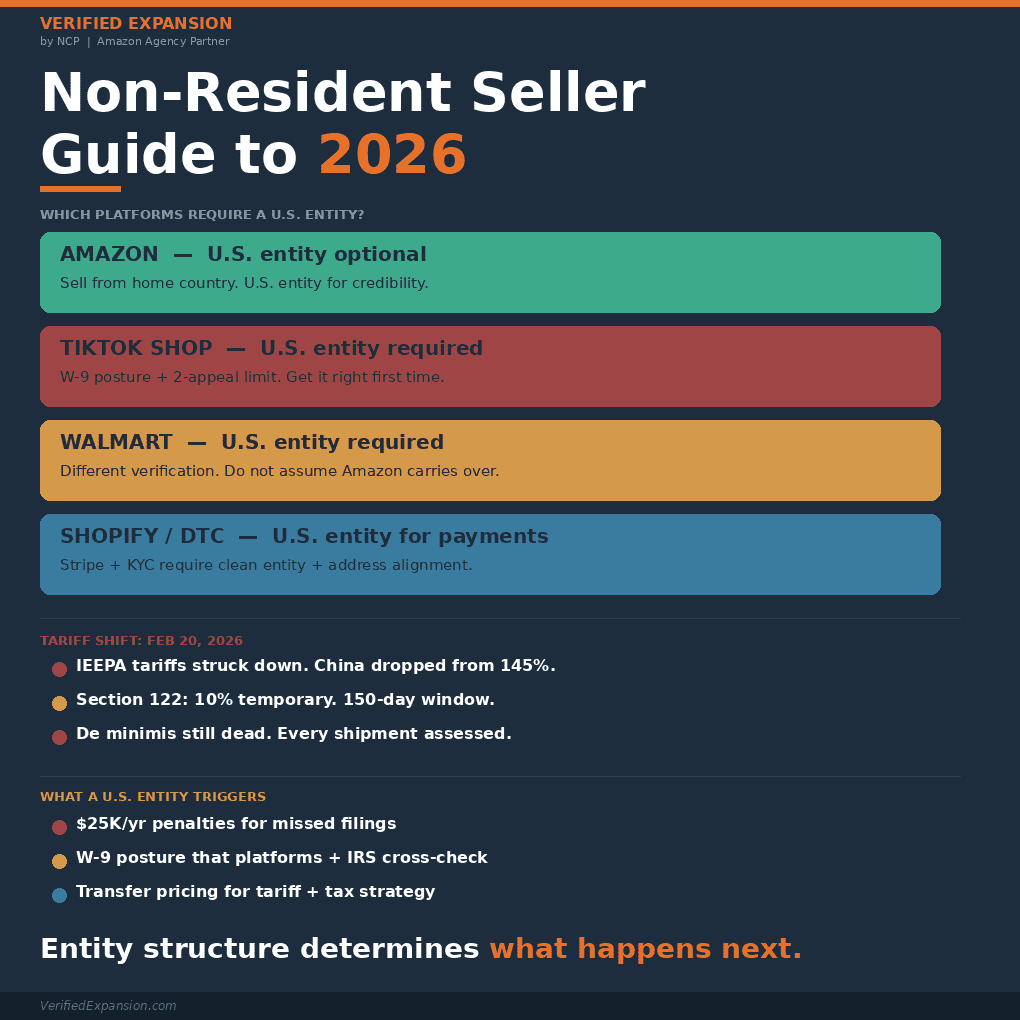

A Non-Resident Ecommerce Seller’s Guide to 2026: Tariffs, Entity Structure, and Marketplace Verification

Your marketplace choice now determines whether you need a U.S. entity, what type of entity, and which compliance obligations come with it. If you are a foreign-owned brand selling in the U.S. in 2026, the rules vary depending on where you sell. Some platforms let you operate from your home country. Others require a U.S. […]

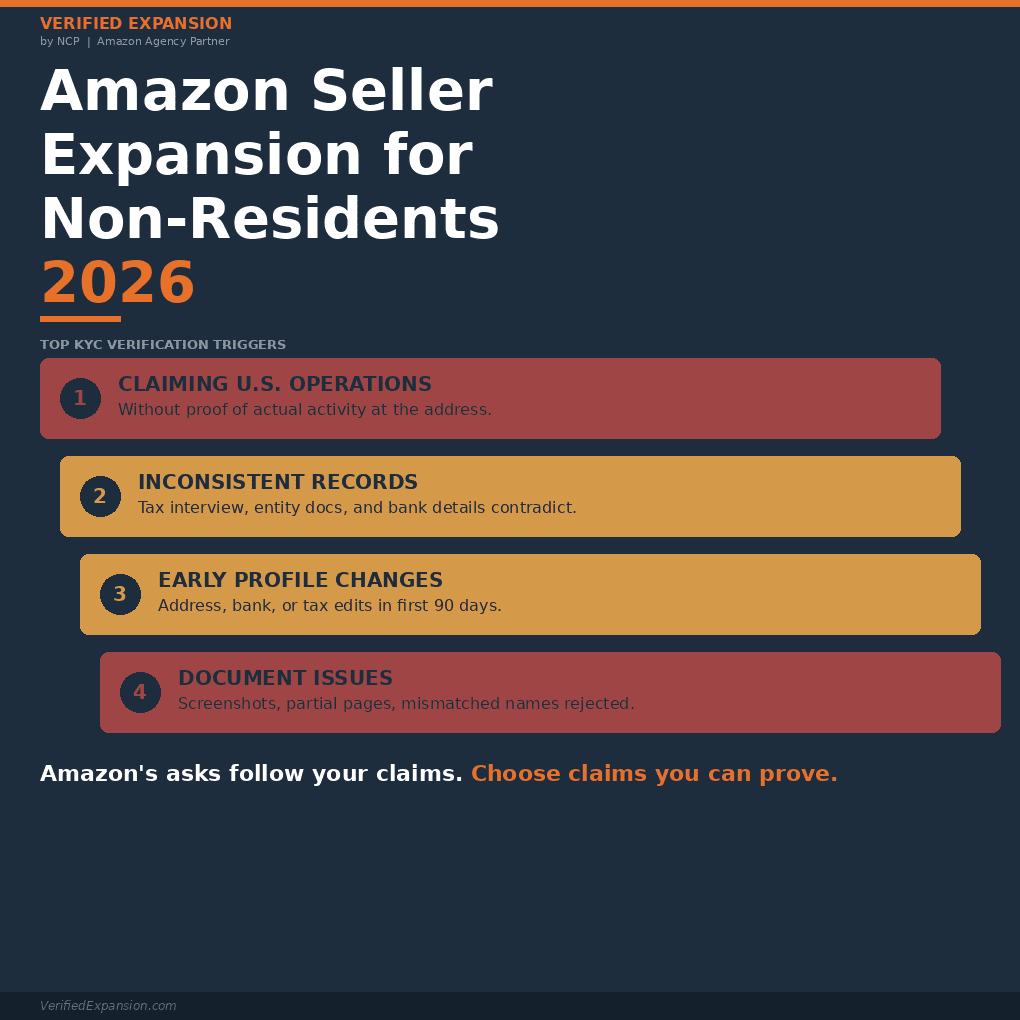

Amazon Seller Account Expansion Strategy for Non-Residents in 2026

Knowing your customer (KYC) is tighter for Amazon in 2026. Set up choices that worked last year now trigger reviews. Amazon’s verification standards have shifted. INFORM Act enforcement is stricter. Document requirements are more specific. And the window for making changes to sensitive fields without triggering a review is narrower than ever. If you are […]

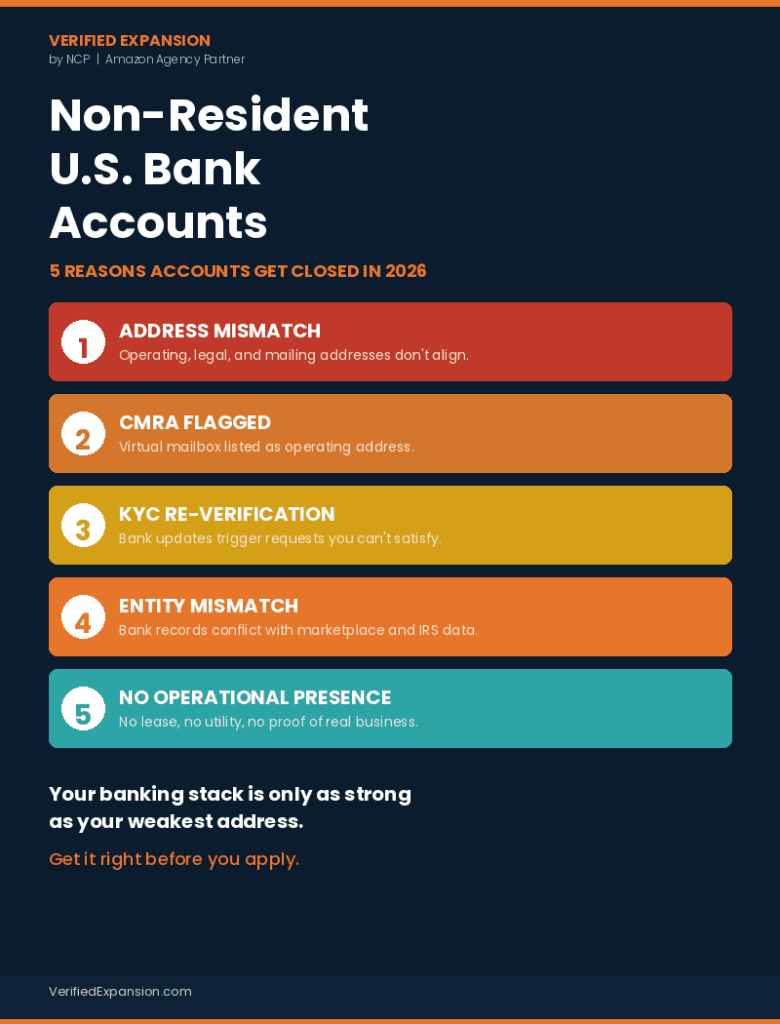

Non-Resident U.S. Bank Accounts: How Compliance Rules Are Shaping Account Options in 2026

Today, non-resident founders must thread three very different needles when looking to establish some “bank account” for their U.S. entity formation. Payout rails used by marketplaces themselves (Amazon’s Currency Converter for Sellers, TikTok Shop Seller Wallet, Walmart Payoneer). Transfer services and neo-banks that sit between you and the customer, such as Wise, OFX, Payoneer, Mercury, […]

Amazon Account Verification: Strategies for Success

The Amazon account verification process is vital to your success on the platform, but it isn’t always easy to navigate. Explore real tips from the experts at Riverbend Consulting to ensure your account verification is successful.

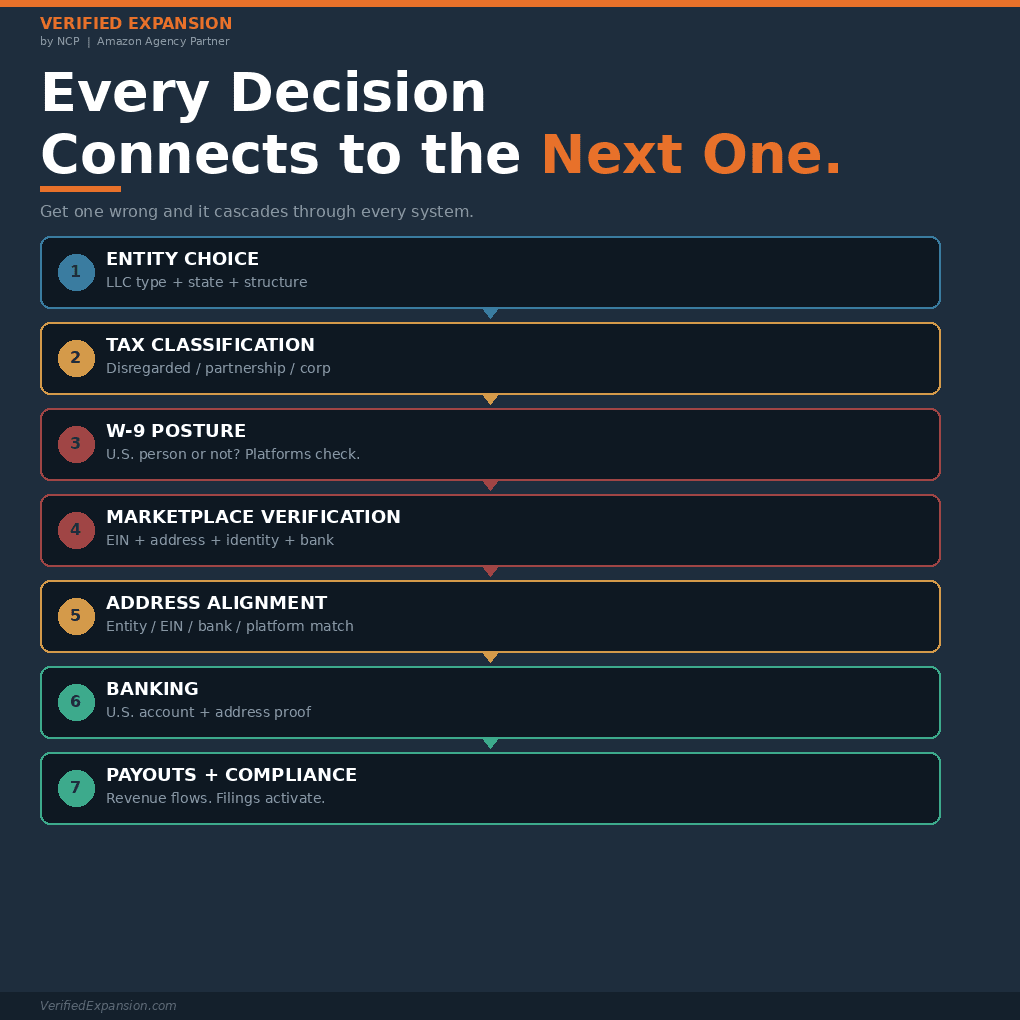

Every Expansion Decision Connects to the Next One. Get One Wrong and It Cascades.

Expanding to the U.S., rewards preparation and punishes shortcuts. These are the questions that separate sellers who launch from sellers who stall. If you are a seven-figure ecommerce brand expanding to the U.S., ambition is not the problem. The problem is that the decisions you make in the first 30 days determine whether you launch […]

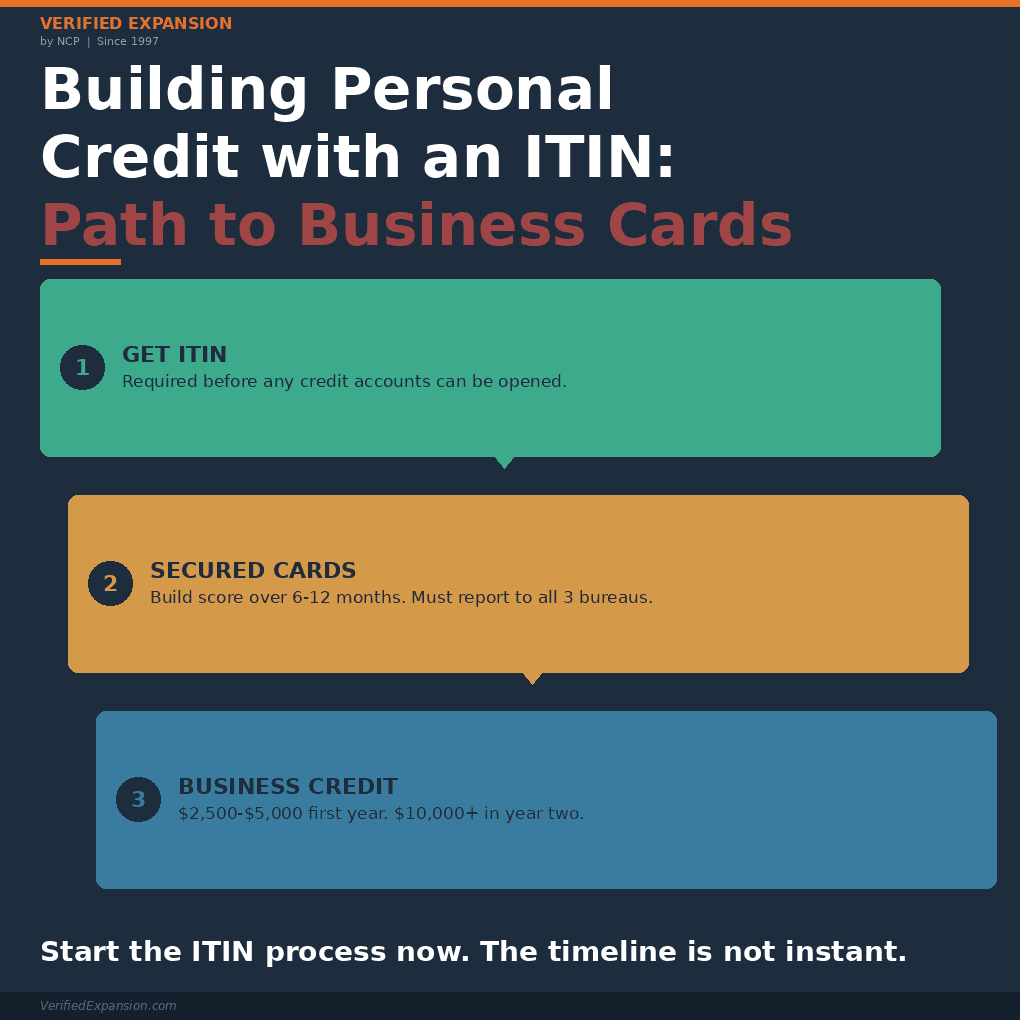

Building Personal Credit with an ITIN: Your Path to Business Credit Cards

Business credit cards require personal credit. Non-residents start at zero. If you are a non-resident with a U.S. entity, you will eventually need a U.S. business credit card. Credit card issuers evaluate your personal credit history before approving a business card, even if your business has strong revenue. Without a personal credit score, you cannot […]

S-Corporation Tax Benefits: An Essential Guide for Business Owners in 2025

Why Choose an S-Corp? For many small business owners, selecting the right business structure can be pivotal. An often underutilized but highly beneficial option is forming an S-Corporation. Here are the top reasons why an S-Corp might be the right choice for your business: Limited Liability Protection Operating as an S-Corp or LLC can protect […]

Corporate Transparency Act Disclosure of Beneficial Ownership Information Impact on Non-U.S. Residents

The Corporate Transparency Act (CTA) is a new federal law requiring most domestic and foreign business entities formed or registered to do business in the United States to disclose information about their beneficial owners to the Financial Crimes Enforcement Network (FinCEN). Update March 2nd: BOI suspended by U.S. Treasury. Learn more here. Update February 27th: […]

How U.S. Banking and Global Payment Platforms have Changed for Non-Residents in 2026

For non-U.S. residents looking to launch a U.S. business, the path to getting a bank account or setting up a payment solution has become more complicated in 2026. Platforms like Wise, Payoneer, and OFX, as well as fintech providers such as Mercury, are tightening their requirements, particularly around entity structure, address verification, and U.S. tax […]

Decoding the W-8BEN: Does It Really Shield You from U.S. Taxes?

A W-8BEN does not mean you owe zero U.S. tax This is the most dangerous assumption non-resident sellers make. A marketplace hands you a W-8BEN during onboarding, and you assume that settles the tax question. It does not. The W-8BEN tells the marketplace how to classify your payments for withholding purposes. It tells the IRS […]

Understanding Amazon’s Tax Interview: Key Mistakes Non-Residents Should Avoid with LLCs

Navigating Amazon’s tax interview for non-residents with U.S. LLC can be complicated, particularly regarding tax compliance. Many non-residents choose to operate as individuals or entities from their home country and will complete the W-8BEN or W-8BEN-E form during the Amazon tax interview. Forming a U.S. single-member LLC often becomes necessary, especially in dropshipping scenarios where […]

Amazon’s Reverification Under the INFORM Consumer Act

As we gear up for the INFORM Consumer Act’s enforcement on June 27, 2023, its impact on Amazon’s reverification process is indisputable. This consumer protection law aims to bolster online transparency, ensure fairness, and hold platforms accountable for their activities. Update June 26th: We would like to inform you that starting July 7th, 2023, Amazon […]

Wyoming LLC Requirements for a U.S. Dropshipping Business

Are you looking to form a Wyoming LLC to establish a dropshipping business in the U.S.? If so, there are many factors to consider, including the legal structure of your business. One popular option for entrepreneurs is forming a limited liability company (LLC) in Wyoming. In this post, we’ll explore the benefits of a Wyoming […]

5472 and Proforma 1120 for a U.S. Single-Member LLC Disregarded Owned by a Non-Resident

If you own a U.S. single-member LLC as a non-resident, the 5472 filing is not optional Non-residents who form a U.S. single-member LLC that is treated as a disregarded entity have an annual IRS filing requirement that most sellers do not know about until it is too late. The penalty for missing it starts at […]

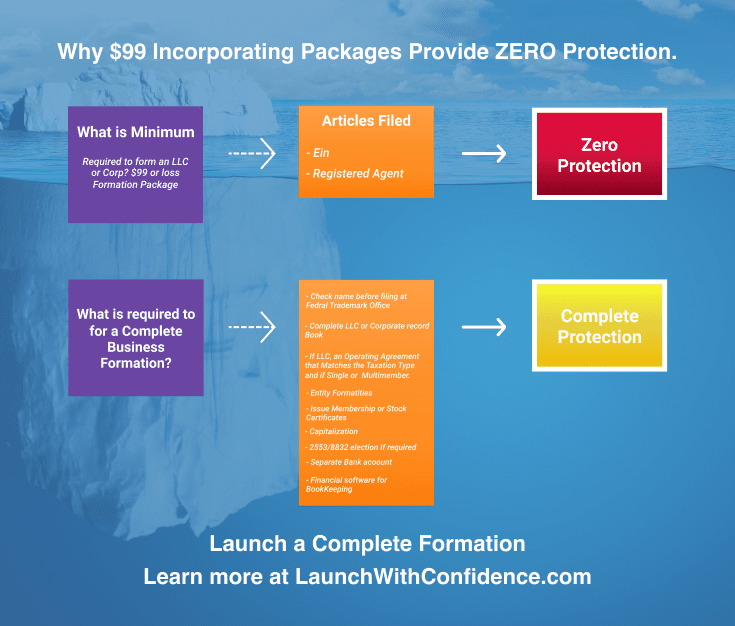

Why a Simple LLC Provides ZERO Protection

If you form a “simple” LLC online with an EIN and a basic operating agreement. With the first legal issue, you may be “financially paralyzed” even if you win the lawsuit! You will not be able to get any loans or financing, which is paramount in today’s economy. What is a “simple” LLC? That is […]

How To Obtain a Sales Tax Exemption Certificate

Suppliers often require an exemption certificate when they ship products from the US. In addition, some B2B marketplaces have created Sales Tax Exemption Programs, such as Amazon (ATEP) and Alibaba (ASTEP), that can quickly help buyers identify as eligible tax-exempt for US sales tax purposes. You may enroll in their program to acknowledge and ensure […]

How to Handle an Amazon Suspension for Insurance Non-Compliance

Keeping your Amazon Seller Central account active is vital to your seller ranking and overall Amazon business. Amazon’s suspension for Insurance non-compliance could happen soon. Ignoring repeated Amazon notices to comply with insurance is not a good idea. Amazon will force compliance and take action for non-compliant people, but the unknown is when. If you […]

Single-Member LLC vs. Multi-Member LLC Charging Order

LLCs are more popular than corporations for a few reasons, including flexibility in the management structure, taxation options, and the bonus of the “charging” order protection in most states. When you operate a business, you must consider what happens if your business is sued directly. Will your business liability insurance policy protect your business assets, […]

Shopify Sales Tax Requirements

Suppose you are selling through Shopify or your own website. In that case, you may have crossed the economic thresholds in several states, which means you must register for a sales tax permit, update your Shopify tax settings (or shopping cart), and collect and remit sales taxes. Even as a non-resident selling in the U.S., […]

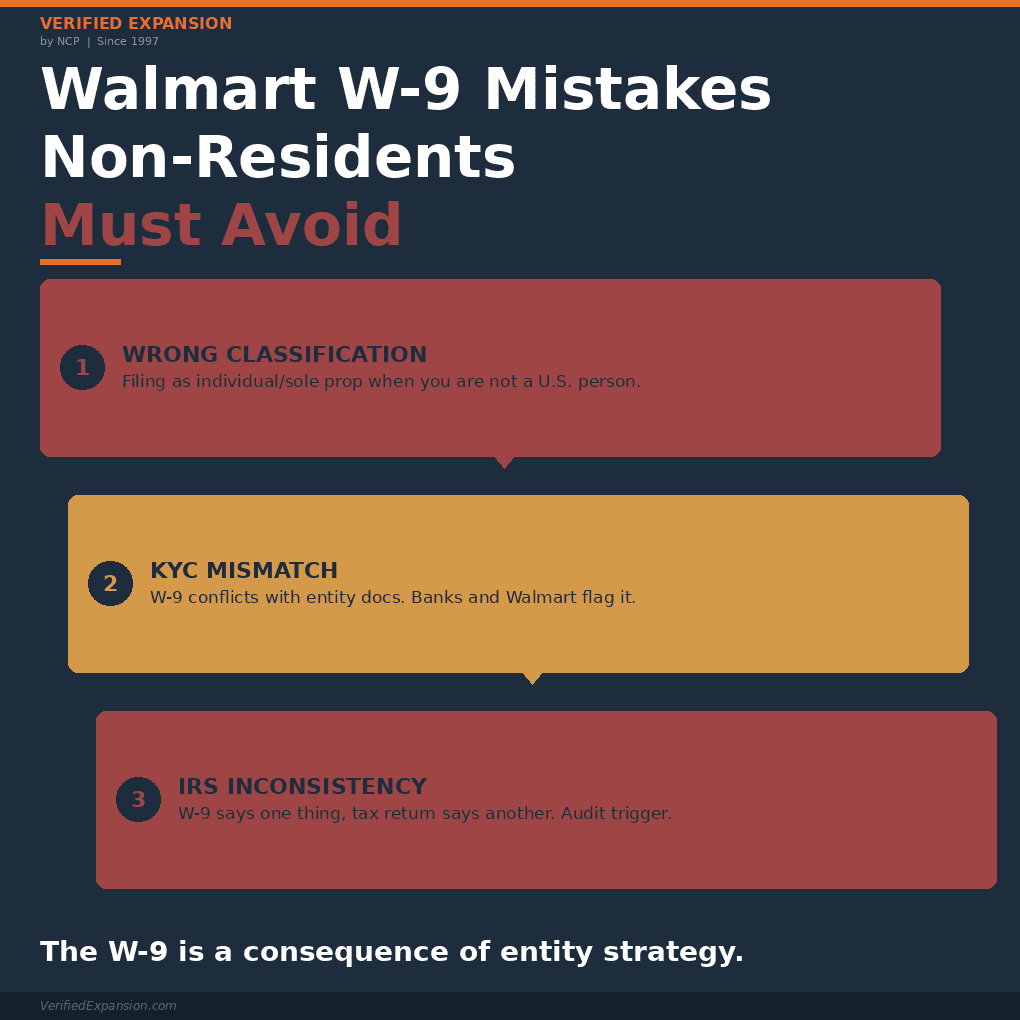

Walmart W-9 Mistakes to Avoid for Non-Residents

The W-9 mistake that can cost your Walmart account and trigger an IRS problem Expanding to Walmart is a natural next step for non-resident sellers who have built traction on Amazon. But the Walmart onboarding process requires a W-9, and the W-9 requires a U.S. entity that files as a U.S. taxpayer. Most sellers get […]

Amazon Seller Insurance Requirements for Non-Resident Sellers

Amazon is now enforcing insurance requirements to sell on their marketplace. Per Amazon’s terms of service, business liability insurance protection is required for all sellers. Do you carry business liability insurance? If not, your Amazon seller account is not protected. Take the steps now to avoid any limited access or account suspension. Don’t drop your […]

How to Protect Your Cryptocurrency From Liability

Cryptocurrency is classified as property by the IRS. Property can be a target of legal action, similar to real estate, and you can lose 100% of your property, or in this case, your cryptocurrency, even if it is DEFI. The blockchain allows the tracing of all transactions involving a given bitcoin address, all the way […]

A Legally Clear Name for Your Business

Every successful business counts on countless good decisions – enough to overcome those that inevitably prove totally wrong. A good business proves itself over and over in its resiliency. I challenge anyone to think of a bigger decision than to find a LEGALLY CLEAR name for your new business or product start-up. A LEGALLY CLEAR […]

U.S. LLC Questions to Ask Before Your E-Commerce Expansion

There are many U.S. LLC questions to ask before formation when you expand your e-commerce business to the U.S. These questions could be more precise. Most sellers only anticipate 1-2 steps ahead (or questions) with their U.S. formation and need to be made aware of these costly mistakes they have already made. Why does this […]

How to Protect Your Corporate or LLC Veil

Learning how to protect your corporate or LLC veil is an important foundation for protecting your personal assets from your business. If you operated your business as a sole proprietorship and sued, you may potentially lose all your personal assets. There is no separation between you personally and your business. This is the simplest form […]

12 Questions to Ask Before and During Forming a U.S. Entity

Forming a U.S. entity correctly is a crucial step to protect your business as it grows for either sale or a profit center to support you and your family. Nothing is worse than building a U.S. brand, working 12+ hours a day to build it up, getting ready to sell, and losing everything because you […]

When to Form Another Entity?

There are a lot of steps to protect your business and your family properly. Here’s a common question that is important that comes up often: “When should I form another entity for my business?” Actually, the more I think about it, that question is not as common as it should be. It is like the quote […]

Coronavirus Financial Survival Strategies

Even with the government’s $2 Trillion aid package, it is key that you have the right information for the best coronavirus financial survival strategies. In a recent interview with Todd Rooker, the #1 financial crisis recovery expert in the U.S., he blew everyone away with very detailed steps that any business owner must take to protect their […]

Sole Proprietors Are Rolling the Dice

Sole proprietors are taking a significant risk in today’s business climate, much more than they have been told. It is time they know the facts and what they are up against to put the odds back in their favor. In today’s ultra-competitive and dangerously litigious business climate, you can’t afford to throw the dice with […]

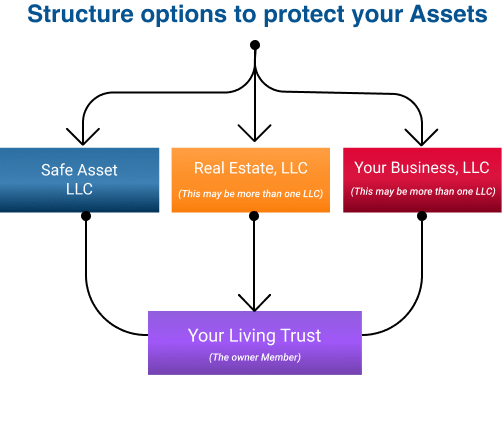

How to Protect Your Safe Assets

Over the years, we have heard the sad stories of clients who had their businesses protected with a separate legal entity. Still, when sued personally, they forgot or never focused on protecting their safe assets (which many times is the savings and investment accounts for their financial future) and lost ALL safe assets. The reasons […]

New Entity or Just File a DBA?

As you grow your product or services with your business, you will come to the point that you may consider forming a new entity or instead just filing a DBA linked to your operating entity. It is one thing to grow a business and your net worth, and it is another to keep it. The […]

How to Protect Your Real Estate Investments

Investing in U.S. real estate is still one of the best investment opportunities loaded with tax advantages. The key is to make sure your real estate is protected beyond just having insurance. When investing in U.S. real estate, it is important to make sure you protect your investments properly. The challenge is real estate has […]

Sly Like a Fox-Asset Protection & Privacy Strategies

Asset protection and privacy is a necessity to protect your wealth in today’s litigious world. There are over 80-million lawsuits in the United States alone each year. Over $200 Billion in frivolous lawsuits every year. In our research, we found a lady that has sued over 700 people during her lifetime. That was her wealth […]

LLC Terms and Definitions

It is important to understand the basic LLC terms and what they mean. You will notice many sounds like corporate terms but keep in mind they are different. Many times, in business situations, people will use inappropriate terms when referring to an LLC. You will come across as more organized and professional when you know […]

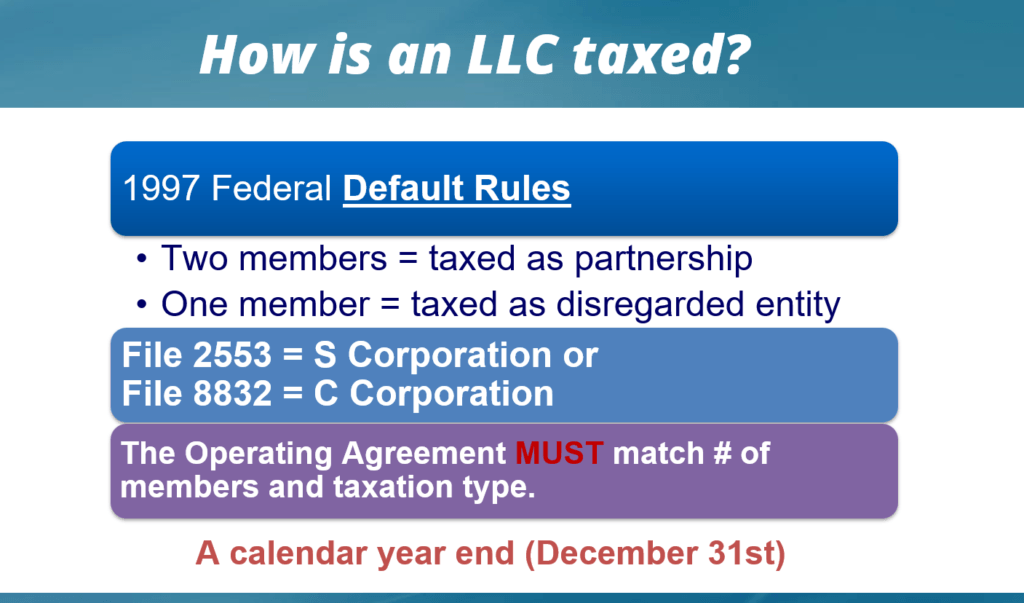

LLC Taxation Case Study

When you form an LLC, you have four options on how it may be taxed, disregarded, S or C corporation, or a partnership. There are a lot of factors to consider which taxation type may be best for your situation. In this case study, we address the key questions you must consider. Here is our […]

Following Corporate Formalities

One of the requirements, when you form a corporation or LLC, is to operate the entity as a separate legal entity from yourself. Corporate formalities are the operating rules and guidelines a corporation must follow to be recognized as a separate legal entity. If corporate formalities are not followed, it is one of the areas […]

LLC Taxation Options: What You Need to Know About Taxes and Distributions

When forming an LLC, choosing how you want to be taxed is one of your most critical decisions. With four taxation options to consider—Partnership, Disregarded Entity, S Corporation, and C Corporation—it’s essential to understand how each one works and its impact on your tax situation. How your LLC is structured, whether member-managed or manager-managed, also […]

Starting a Business as a Sole Proprietorship; Good or Bad Idea?

A sole proprietorship is the simplest form of business. It’s not a separate entity. Instead, as a sole proprietor, you own the business and are directly responsible for its debts. Remember that whenever you do something the “simplest” way, it’s typical for your results to be directly proportional to the effort required. It is the […]

Benefits of Incorporating Your Business

There are several benefits of incorporating your business, including separating your business liability from your personal assets, your personal and business credit, and potential tax savings depending upon levels of profits. Here are additional benefits of incorporating your business that most don't consider but should to grow your business. The benefits of incorporating include increasing [...]

How to Start a Company in the U.S.

Mastering the art of starting a company in the U.S. is the ultimate key to unlocking your company's full potential in the American e-commerce scene. By doing so, you open up a world of opportunities to maximize your business's value, from joint ventures and affiliate sales to investments in lucrative U.S. real estate and tax [...]

Asset Protection for the Cannabis Industry

If there is any industry where you want to make sure you have extra layers of protection for your business and personal assets, it’s the cannabis (CBD oil) industry. The U.S. is the land of opportunity and also the land of lawsuits. We have more lawsuits than any other country in the world. Selling products […]

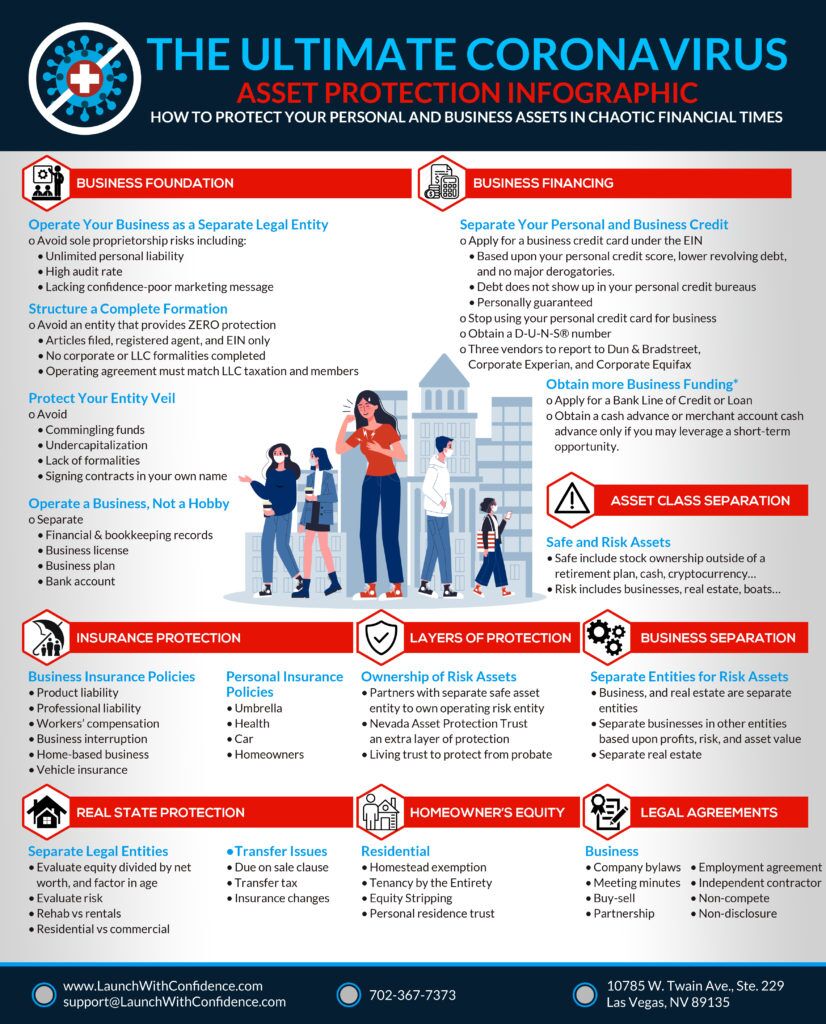

Asset Protection Infographic

You need to protect your assets, especially during difficult times such of when the country was shut down during the pandemic due to COVID-19 or now with rising interest rates and higher inflation. The fragile economic conditions are a strong signal to protect your assets now before it is too late. Many businesses had to […]