You bought the TikTok Shop liability insurance policy. You filed the LLC. You launched your creator program. You are still exposed.

Having a Policy Is Not the Same as Being Protected.

A foreign brand forms a U.S. LLC and files it online. Applies to TikTok Shop. Activates thirty creators. Buys a product liability policy.

They believe the risk is handled.

It is not.

Having a policy and being protected in practice are two different things. The gap between them is exactly where financial damage lives. In beauty and supplements on TikTok Shop, that gap is wider than most founders realize until the moment it matters most.

Amazon requires product liability insurance when a seller exceeds $10,000 in monthly sales. TikTok Shop has no equivalent mandate. Most brands read that as good news. It means thousands of brands are operating with full legal exposure and zero external pressure to close the gaps.

The brands that get hurt are not the ones that ignored compliance entirely. They are the ones who did just enough to feel protected without doing enough to actually be protected. That is the dangerous middle. TikTok Shop is full of it right now.

One Claim. Three Places It Hits at Once.

When something goes wrong on TikTok Shop, the sequence compresses fast. A consumer complaint becomes a platform review. Payouts freeze. The account goes under investigation. The brand cannot sell and cannot withdraw funds. That is before a single demand letter arrives.

In beauty and supplements, the claim is rarely limited to the product alone. It can involve what was said about the product, what a creator claimed, what was omitted, and who presented themselves as responsible for the business. By the time a brand discovers which coverage applies and who qualifies as an insured, the damage is already underway.

The real question is never just: do you have insurance? The real question is: if a large claim hits, what exactly is covered, who actually qualifies as an insured, and does the policy respond within the limits you think you bought?

The Case Law Is Moving. The Trends Are Clear.

Courts and regulators are increasingly willing to scrutinize platform responsibility in the third-party seller chain. Outcomes vary by jurisdiction and claim theory, but the direction is consistent: when a claim lands, the platform points back to the seller of record.

Active class actions are moving through federal court, targeting supplement brands for health and performance claims that outrun regulatory requirements. The case law in beauty is generating new litigation pressure around ingredient claims, natural and clean marketing, and product performance representations.

These are not fringe cases. They are the pattern your brand is operating inside right now.

The brands at risk are not the ones that ignored compliance entirely. They are the ones that launched with a product liability policy and assumed the rest would sort itself out.

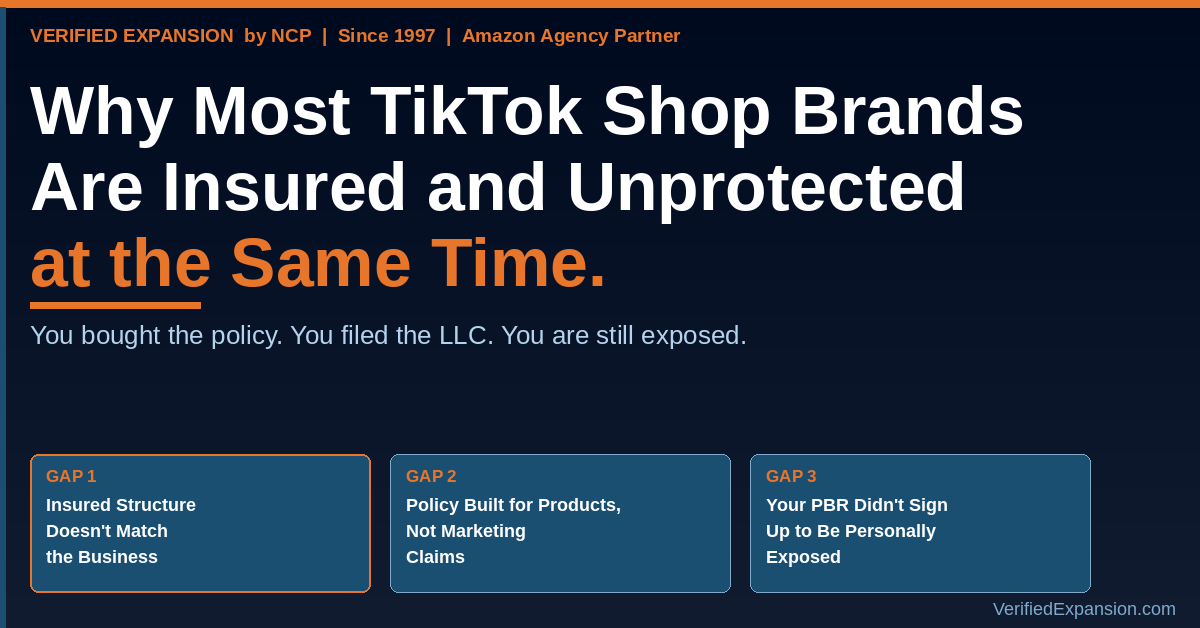

Gap 1: The Insured Structure Does Not Match the Business

Filing an LLC is the beginning of protection, not the end of it. In a serious claim, whether the right entity and the right people are actually named as insureds becomes critical quickly.

Being associated with the company is not the same as qualifying as an insured under the policy wording. Most people in visible roles have never confirmed that distinction.

Gap 2: The Policy Was Built for Product Claims. The Real Exposure Comes From Marketing Claims.

A product liability mindset alone is too narrow for TikTok Shop. The highest-risk events in beauty and supplements often start in the marketing layer, not the product layer. What creators say, what affiliates claim about competitors, and what health or performance language appears in content creates exposure categories that a standard product liability policy was not designed to address.

Some of those claims fall entirely outside the policy. Some implicate different coverage parts. Some are not insurable, as founders assume. Treating product liability as if it covers the entire creator economy risk stack is the most common and most costly mistake in this category.

How a brand describes its business and creator program to a carrier matters as much as which policy it buys. A brand that looks like a simple product seller on its application, but operates an active affiliate and influencer program with health claims, is not the risk the carrier priced.

Gap 3: The Person Named on Your Account Did Not Sign Up for This

Every TikTok Shop seller account has a Primary Business Representative. That is the individual whose identity is verified and whose name is attached to the platform account. For many foreign-owned brands, that person accepted the role without fully understanding what it means when something goes wrong.

Whether that individual is protected depends heavily on how the entity was formed, what the policy says about insured status, and what role they were actually performing when the event occurred. Most PBRs and the brands they represent have never had that conversation.

Protection Is Not a Policy. It Is a Structure.

The brands that come through serious claims intact are the ones whose entity, policy, insured structure, creator program, and operating facts all lined up before the first incident. That alignment does not happen automatically. It has to be built before the first sale, not after the first problem.

Protecting your brand on TikTok Shop is one component of comprehensive U.S. expansion planning. It connects to your entity structure, your verification sequence, your tax posture, and the people tied to your account.

Most brands find out what is missing after the first incident.

The CEO Blueprint was built so you can find out before.

Frequently Asked Questions

Does TikTok Shop require product liability insurance?

TikTok Shop does not appear to impose a universal product liability requirement on every seller the way Amazon does. That does not reduce the seller’s legal exposure. A platform requirement and an actual risk requirement are not the same thing.

Why is product liability insurance alone often not enough for TikTok Shop beauty and supplement brands?

Because the highest-risk events in this category often start in the marketing layer. Creator content, affiliate comparisons, health and performance claims, and disclosure failures create exposure that a standard product liability policy was not designed to address. Some of those claims fall entirely outside the product liability grant.

What is a TikTok Shop Primary Business Representative, and why does it matter?

The PBR is the individual whose identity is verified and whose name is attached to the seller account. Whether that person qualifies as an insured under the brand’s policy depends on the policy wording, the entity structure, and their actual role. Most PBRs and the brands they represent have never confirmed that status.

What is the difference between a TikTok Shop affiliate and a TikTok Shop influencer?

A TikTok Shop affiliate drives sales through a tracked commission link and earns per sale. A TikTok Shop influencer typically receives a fixed fee plus commission and operates under a longer-term brand partnership. Both create legal exposure for the brand’s U.S. entity based on what the creator says and fails to disclose.

What does the CEO Blueprint cover for TikTok Shop brands?

The CEO Blueprint is a comprehensive U.S. expansion planning covering entity structure, tax exposure, verification sequencing, insurance category review, PBR, and authorized representative protection, and specialist referrals. Two strategy calls with Scott Letourneau and a written plan built around your specific facts.

Disclaimer: Educational purposes only. Not legal, tax, or insurance advice. Insurance coverage depends on specific policy language, underwriting facts, jurisdiction, and claim circumstances. Consult qualified legal counsel and a licensed insurance professional for guidance specific to your situation.